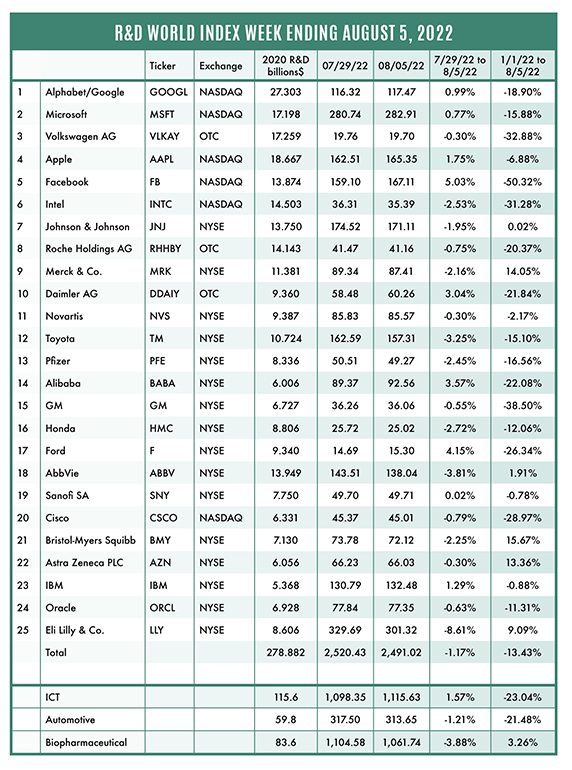

The R&D World Index (RDWI) for the week ending August 5, 2022 closed at 2,491.02 for the 25 companies in the RDWI. The Index was down -1.17% (or -29.41 basis points) from the week ending July 29, 2022. Nine of the 25 RDWI members gained value from 0.02% (Sanofi SA) to 5.03% (Facebook/Meta Platforms Inc.). Sixteen of the 25 RDWI members lost value last week from -0.30% (Astra Zeneca PLC, Novartis and Volkswagen AG all tied at -0.30%) to -8.61% (Eli Lilly & Co.).

The R&D World Index (RDWI) for the week ending August 5, 2022 closed at 2,491.02 for the 25 companies in the RDWI. The Index was down -1.17% (or -29.41 basis points) from the week ending July 29, 2022. Nine of the 25 RDWI members gained value from 0.02% (Sanofi SA) to 5.03% (Facebook/Meta Platforms Inc.). Sixteen of the 25 RDWI members lost value last week from -0.30% (Astra Zeneca PLC, Novartis and Volkswagen AG all tied at -0.30%) to -8.61% (Eli Lilly & Co.).

Click to enlarge.

RDW Index member Oracle Corp., Austin, Texas, announced last week that it laid off several hundred employees, which primarily were in their advertising and customer experience groups. The cuts came as the company increases its focus on cloud-based healthcare services following regulatory approval for its $28.3 billion purchase of electronic-medical-records company Cerner Corp., North Kansas City, Missouri. Some layoffs were also announced for Cerner as part of the integration of that company into Oracle. Cerner had expected 2020 R&D investments of about $600 million while Oracle spent more than $6 billion in R&D in 2020.

RDW Index member Pfizer, New York City, announced last week that it is in advanced talks to acquire Global Blood Therapeutics Inc., South San Francisco, for about $5 billion, although other suitors are also considering GBT. GBT recently was approved for the manufacture of a drug for sickle cell anemia. Pfizer is looking to add about $25 billion in new products to its portfolio through mergers and acquisitions by 2030.

Amgen, Thousand Oaks, California, last week agreed to acquire ChemoCentryx, San Carlos, California, for about $4 billion. ChemoCentryx is a biotech company with a recently approved drug to treat a rare immuno-system disease. The Pfizer and Amgen deals are expected to augur more biotech deals with a $40 billion Merck-Seagen deal being considered for cancer drugs.

Tesla, Austin, Texas, announced last week that the company is likely to need about a dozen factories to reach its goal of selling 20 million electric vehicles (EVs) annually by 2030. The company stated that it expects to manufacture 1.5 to 2.0 million EVs annually at each of its factories. Tesla currently has four operating factories.

OrganEx Inc., Cambridge, Ontario, Canada, revealed last week in a paper published in the journal Nature that the company had restored function to the organs of dead pigs. This raises hopes that a similar process could make more human organs available for transplantation in the future in such applications as kidneys, livers, hearts and other organs.

Germany last week said that due to the Russia-Ukraine war and the resulting reduction of natural gas being shipped to Europe following sanctions against the Russian invasion, that the government is reconsidering its 20-year-old decision to close all its nuclear reactors. The three remaining reactors generate about 6% of Germany’s electricity. Most Germans approve of extending the life of the reactors and tests are now underway to evaluate their usefulness. A gas turbine built to improve the Russian gas flow has been refused for acceptance by Russia.

China’s leading EV battery manufacturer, Contemporary Amperex Technology Co., has postponed indefinitely its decision to build a battery factory in the U.S. due to political tensions between the U.S. and China. No decision is expected to be made before late-September.

The U.S. Department of Labor announced last week that U.S. employers added a strong 528,000 new jobs in July, despite a slowdown in the U.S.’s overall economy. The U.S. job market has now almost fully recovered from its loss of 22 million jobs at the beginning of the COVID-19 pandemic in early 2020. However, there are still 623,000 fewer people in the U.S. workforce, which has pushed up wages (and inflation) due to increased demand. The Department of Labor also reported last week that U.S. job openings fell in June to their lowest level in nine months, 10.7 million, down from 11.3 million in May.

The Institute for Supply Management, Tempe, Arizona, last week reported that its index of factory activity came in at 52.8 in July, down slightly from 53.0 in June, but still above the 50.0 break point that might signal a recession. Activity continues to grow slowly among American manufacturers, but it continues to grow. The U.S. Department of Commerce also reported last week that the U.S. economy contracted in 2Q, after contracting in 1Q. Consumer demand for manufactured goods also continues to decline, but many of those goods are not manufactured in the U.S.

Advanced Micro Devices (AMD), Santa Clara, California, announced last week, a 70% increase in 2Q sales from a year ago. The company also forecast subdued sales for the 3Q, which fell below analysts’ expectations. Most of AMD’s 2Q growth was focused on its data-center business sector, an area where strong competitor Intel has stumbled. Intel also forecast a lower full-year sales outlook last week, siting delayed delivery of manufacturing equipment and systems.

China’s LONGi, Xi’an, last week announced that its central R&D institute officially started operations at the company’s headquarters. The institute incorporates a high efficiency monocrystalline cell center with a pilot production line for its next generation of new products. LONGi is ranked as China’s 12th largest new economy enterprise.

R&D World’s R&D Index is a weekly stock market summary of the top international companies involved in R&D. The top 25 industrial R&D spenders in 2020 were selected based on the latest listings from Schonfeld & Associates’ June 2020 R&D Ratios & Budgets. These 25 companies include pharmaceutical (10 companies), automotive (6 companies) and ICT (9 companies) who invested a cumulative total of nearly 260 billion dollars in R&D in 2019, or approximately 10% of all the R&D spent in the world by government, industries and academia combined, according to R&D World’s 2021 Global R&D Funding Forecast. The stock prices used in the R&D World Index are tabulated from NASDAQ, NYSE and OTC common stock prices for the companies selected at the close of stock trading business on the Friday preceding the online publication of the R&D World Index.

Tell Us What You Think!