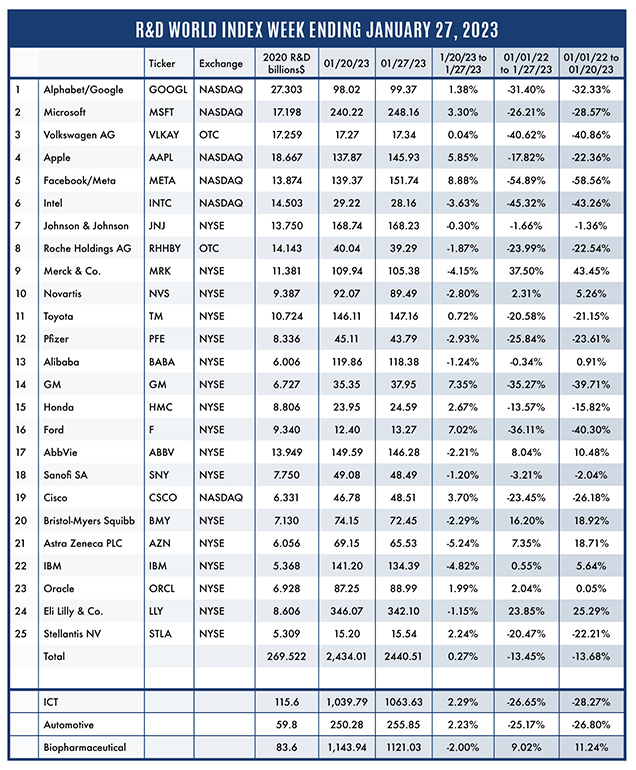

The R&D World Index (RDWI) for the week ending January 27, 2023, closed at 2,440.51 for the 25 companies in the RDWI. The Index was up 0.27% (or 6.50 basis points) from the week ending January 20, 2023. Twelve of the 25 RDWI members gained value during the past week from 0.04% (Volkswagen AG) to 8.88% (Facebook/Meta Platform). Thirteen of the 25 RDWI members lost value last week from -0.30% (Johnson & Johnson) to -5.24% (Astra Zeneca PLC).

The R&D World Index (RDWI) for the week ending January 27, 2023, closed at 2,440.51 for the 25 companies in the RDWI. The Index was up 0.27% (or 6.50 basis points) from the week ending January 20, 2023. Twelve of the 25 RDWI members gained value during the past week from 0.04% (Volkswagen AG) to 8.88% (Facebook/Meta Platform). Thirteen of the 25 RDWI members lost value last week from -0.30% (Johnson & Johnson) to -5.24% (Astra Zeneca PLC).

Click to enlarge.

The German government last week announced that its economy is expected to expand 0.2% in 2023, revising a -0.4% contraction the government forecast about six months ago. The contraction was initially expected to be as much as -12% following Russia’s attack on Ukraine and the resulting energy crunch it created. The current expectation is that the expected recession will now be shorter and milder “if it takes place at all.” A warm winter and heavy government spending to shield businesses and households from high prices and energy-saving measures minimized those initial fears. However, a period of low growth is still expected.

Multinational software company SAP SE, Walldorf, Germany, announced job cuts last week of up to 3,000 positions following a steep drop in profits in late 2022. SAP was expected to invest more than $5 billion in R&D in 2020. The planned SAP job cuts will affect about 2.5% of the company’s workforce, which totaled about 110,000 at the end of 2022. SAP also stated that they are looking for a buyer of its Qualtrics International division which tracks customer interactions with its software. Even with a major contract with German automotive company BMW AG, the software division has continued to decline since its acquisition in 2021.

Chemical manufacturer, Dow Inc., Midland, Michigan, announced last week that it is laying off about 2,000 employees globally and is targeting a $1 billion reduction in costs for 2023 following a drop-off in sales demand. Dow was expected to invest about $2.5 billion in R&D in 2020. The company is looking to shut down certain assets and align spending with the macroenvironment.

Boeing Co., Arlington, Virginia, announced last week that it plans to hire about 10,000 employees in 2023, about half the number it hired in 2022. The company hired more in 2022 as it fought against attrition and worked to boost deliveries of its 737 MAX and 787 jetliners. Boeing competitor Airbus SE, Leiden, Netherlands, announced last week that it plans to hire more than 13,000 new staffers in 2023 — a similar number to what it hired in 2022 — to accelerate production of its commercial jets, recover from escalating delivery delays and meet surging demand for new aircraft.

The U.S. Food and Drug Administration (FDA), Silver Spring, Maryland, proposed last week that it would like to simplify the nation’s COVID-19 vaccine procedures with people getting one shot annually. That vaccine would target Omicron and the original strain of the coronavirus. It would streamline a complicated regimen of initial vaccinations and subsequent booster shots.

The Federal Reserve is expected to continue to slow interest rate increases at its first 2023 meeting this week on January 31 – February 1, to a more traditional quarter point which would give the fed governors more time to assess the impact of their increases to establish a stopping point. The new increase would bring the rate to a peak of between 4.5% and 4.75%. The next Fed meeting is scheduled for the end of March and analysts expect that that meeting would see the last rate increase for the foreseeable future. The slowing interest rate increases match the slowing inflationary rate data.

Electric vehicle (EV) manufacturer Tesla, Austin, Texas, announced last week that it would invest more than $3.6 billion to expand its EV plant near Reno, Nevada. The expansion would include its lithium-ion battery and associated EV component facilities and add 3,000 employees. One of these facilities would be targeted at mass-producing Tesla’s semitrailer truck while two others would be focused on making enough batteries for two million passenger vehicles annually. Tesla has stated that it might open 10 to 12 new factories to increase EV production to meet its goal of selling 20 million EVs annually by 2030.

RDW Index member Ford Motor Co., Dearborn, Michigan, announced last week that it is in talks with Chinese EV manufacturer BYD Co., concerning the sale of Ford’s automotive plant in Saarlouis, Germany. Ford has announced the end of its production of conventional automobiles in Saarlouis and its future EV production build-up in Valencia, Spain. BYD’s purchase of the Saarlouis plant would create a European bridgehead for its EV production.

RDW Index member, Johnson & Johnson, New Brunswick, New Jersey, announced last week that it is on track to have its consumer-health business become independent in 2023. This separation will allow the company to focus on its higher growth divisions, namely med-tech and pharmaceuticals. Its consumer business, which will be named Kenvue, will include the acetaminophen Tylenol and ibuprofen Motrin analgesics.

RDW Index member Intel Corp., Santa Clara, California, reported a fourth quarter 2022 loss last week which was hurt by a declining market for its semiconductor devices and increasing competition from rivals, like Advanced Micro Devices (AMD) and British chip specialist ARM Ltd. Intel expects to post another loss for its 1Q 2023. These sales results come following Intel’s decision to expand its very expensive production base. Poor market conditions for Intel are expected to last throughout 2023.

R&D World’s R&D Index is a weekly stock market summary of the top international companies involved in R&D. The top 25 industrial R&D spenders in 2020 were selected based on the latest listings from Schonfeld & Associates’ June 2020 R&D Ratios & Budgets. These 25 companies include pharmaceutical (10 companies), automotive (6 companies), and ICT (9 companies) which invested a cumulative total of nearly 260 billion dollars in R&D in 2019, or approximately 10% of all the R&D spending in the world by government, industries, and academia combined, according to R&D World’s 2021 Global R&D Funding Forecast. The stock prices used in the R&D World Index are tabulated from NASDAQ, NYSE, and OTC common stock prices for the companies selected at the close of stock trading business on the Friday preceding the online publication of the R&D World Index

Tell Us What You Think!