The R&D Tax Credit offers a significant tax incentive for companies in a broad spectrum of technology-based industries. The credit has been part of the Internal Revenue Service tax code since 1981 and is responsible for billions of dollars in tax savings each year. It has gained even more popularity as a result of modifications included in the Protecting Americans from Tax Hikes Act (PATH) of 2015. Along with making the credit permanent, the PATH Act also allowed the R&D Tax Credit to offset alternative minimum tax (AMT) for certain eligible small businesses, which in previous years was a significant restriction for many taxpayers.

Additionally, start-up businesses can now opt to apply the credit against FICA payroll tax liabilities up to $250,000 for up to five years. The value of this tax incentive is undeniable but determining eligibility to claim the credit can be confusing. The code section that addresses funded research has been historically interpreted by taxpayers inconsistently, giving the credit a reputation as one of the most abused sections in the revenue code.

Determining eligibility for the credit requires understanding the concept of “funded research” and reviewing the case law over the years that has helped to shape and define this issue. Each year there are new court rulings which can help sharpen our understanding of this topic. As such, pairing an understanding of the “spirit” of the law with thorough documentation is crucial for any R&D Tax Credit claim.

Contract funding scrutinized

IRS challenges around funded research are interpreting this portion of the federal revenue code.

IRC section 41(d)(4)(H) provides that qualified research excludes “[a]ny research to the extent funded by any grant, contract or otherwise by another person (or governmental entity)”.

What does it truly mean for the research to be “funded by” a third party? Courts have held that the issue can be broken down into two components — Risk and Rights.

If a contract stipulates that the taxpayer is required to succeed or return the funds, or if the taxpayer incurs additional costs beyond what the client is paying, the taxpayer is at some level of financial risk.

For example, the research process typically begins in the pre-award (or bid and proposal) phase. As pre-award work is typically self-funded, research expenses associated with these efforts may qualify towards the research credit. Along the same lines, internal R&D (IR&D) efforts may also qualify. The project team needs to document their time and the specific nature of this research to support tax credit eligibility later.

Contract types generally excluded from the research credit are:

- Cost plus

- Time and materials (incl. hourly)

- Cost plus fixed fee

Contract language requires due diligence

Contract language can be nuanced. The matter of payment and the terms of payment are key aspects of due diligence to support R&D credit eligibility.

In the tax court case of Populous Holdings, Inc. v. Commissioner of Internal Revenue Service (2019), the IRS held the position that the research by Populous was funded and therefore ineligible for the R&D credit.

However, in this case the U.S. Tax Court granted summary judgment to Populous, concluding that payment was contingent upon the success of the research, which put Populous at risk for nonpayment. The court also agreed that Populous retained substantial rights to the research. This case is consistent with court precedent that “risks and rights” play heavily into considerations for claiming the R&D credit.

Missing documentation derails credit eligibility

To determine eligibility for the R&D credit, a contractor must apply the four-part test as outlined in the federal revenue code. It is summarized as follows:

- Elimination of Uncertainty: Changes for aesthetic reasons do not qualify, but research that tangibly improves the product or service could quality. There must be some technical uncertainty at the outset of the job which is eliminated through the process of engineering and design. The R&D process is the “proving out” of the concept until all uncertainty has been eliminated.

- Process of Experimentation: The research must demonstrate that the taxpayer has evaluated alternatives for achieving the desired results.

- Technological in Nature: The process of experimentation relies on hard sciences, such as engineering, physics, chemistry, biology or computer science.

- Qualified Purpose: Show that the purpose of the research was to create a new or improved product or process, resulting in increased performance, function, reliability or quality.

In Siemer Milling Company v. Commissioner of Internal Revenue Service, the outcome was very different from Populous and hinged on documentation rather than the funding source. The IRS concluded that Siemer was not eligible for the R&D credit that the company claimed over two tax years.

Although the U.S. Tax Court agreed that the business components met the requirements of IRC Section 41, the court could not confirm the company’s (2) Process of Experimentation or its hard scientific principles to prove that the research was (3) Technological in Nature. Lack of detailed documentation in these two areas led the court to rule in favor of the IRS.

This case reveals the importance of detailed documentation during pre-award research all the way through project completion.

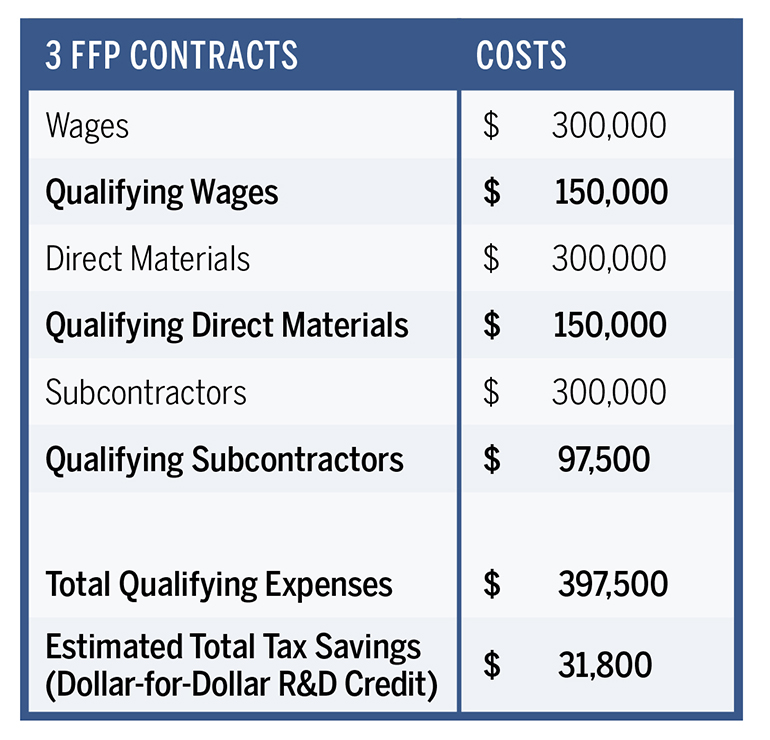

Example: Within a company’s contract mix, they have three firm fixed price contracts where payment from the customer is contingent on success of the research and development activity. Each contract has at least $100K of wages, direct materials and subcontractor costs. On each of the jobs, only 50% of the wages, supplies and contract research meet the “Four Part Test” criteria. That level of R&D spending could produce a tax credit in the range of $25,000 to $40,000.

As you can see in this example, there are several variables to determining the R&D credit. After identifying all qualifying costs, a business owner can generally expect a dollar-for-dollar tax credit of 7-9% of that total. Again, with proper documentation of eligible costs and careful calculation, the potential tax savings can be substantial.

As you can see in this example, there are several variables to determining the R&D credit. After identifying all qualifying costs, a business owner can generally expect a dollar-for-dollar tax credit of 7-9% of that total. Again, with proper documentation of eligible costs and careful calculation, the potential tax savings can be substantial.

Don’t rule out tax credit eligibility

Federal or state grants or contracted funding for research do not necessarily exclude a taxpayer from eligibility for R&D credits. Careful contract negotiation, thorough documentation and an understanding of qualified expenses can lead to thousands of dollars in tax savings — and cash flow for future research.

Upon meeting the four-part test, a company’s qualified expenses are limited to:

- Taxable wages for employees who perform or directly supervise or support qualified activities

- Cost of supplies used in qualified activities, including extraordinary utilities, excluding capital items or general administrative supplies

- Up to 65% of contract research expenses for qualified activities, provided the taxpayer retains substantial rights

The intention of the R&D Tax Credit is to support research for innovative products and improvements in a variety of industries, and to incentivize companies for taking risks that promote technological advancements. To qualify, taxpayers must establish and sustain a system of due diligence and documentation for qualified expenses just as carefully as the research they conduct.

Christopher D. Cook, CPA, is with Anglin Reichmann Armstrong CPAs and Business Advisors, with offices in Huntsville, Ala., and Pensacola, Fla. Cook has a special focus on government contractors and the R&D Tax Credit. [email protected]

Tell Us What You Think!