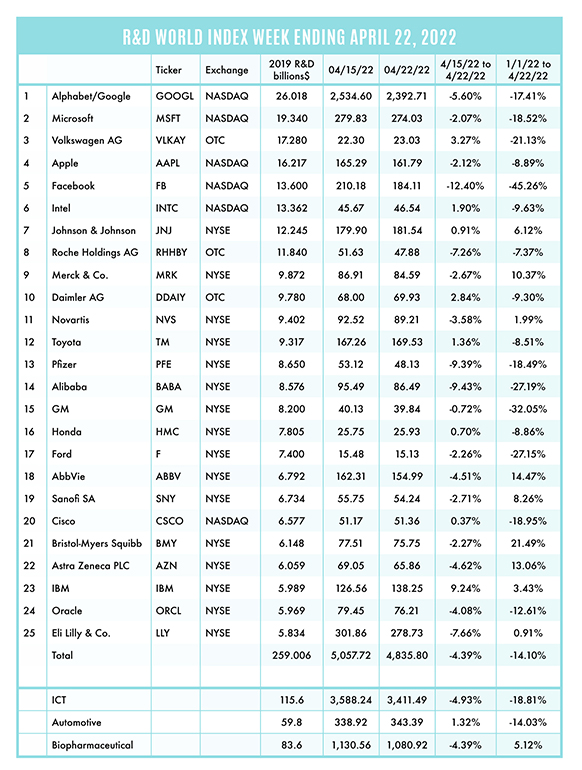

The R&D World Index (RDWI) for the week ending April 22, 2022, closed at 4,835.80 for the 25 companies in the RDWI. The Index was down -4.39% (or 221.92 basis points) from the week ending April 15, 2022. Eight of the 25 RDWI members gained value from 0.37% (Cisco) to 9.24% (IBM). Seventeen of the 25 RDWI members lost value from -0.72% (General Motors) to -12.40% (Facebook).

Click to enlarge.

Toshiba Corp., Tokyo, announced last week that it was putting itself up for auction and stated that it would solicit and consider bids from investors who want to take the company private. This action follows attempts by executives to split the company into two or three parts which were rebuffed by shareholders. The company has struggled following 1) an accounting scandal in 2015, 2) the bankruptcy of its U.S. nuclear-energy division, Westinghouse Electric Company in 2017, which was then acquired by Brookfield Business Partners, Toronto, in 2018, and 3) the disclosure of broad collusion between the company and the Japanese government in 2021. Toshiba said it would seek non-binding proposals and finish an initial evaluation before its annual shareholder meeting in June. After the shareholder meeting, the company plans to solicit binding proposals and then select the best one. Toshiba has R&D centers in Japan (Kawasaki-shi), China (Beijing), India (Bangalore), the UK (Cambridge and Bristol) and the U.S. (New York City). The company invested more than $1.8 billion in R&D in 2020. The company was founded in 1875 and currently has more than 140,000 global employees.

Confectioner Mars Wrigley, Chicago, a division of Mars Inc., McLean, Virginia, announced last week that it would build a new $40 million R&D facility on the near-north site of its global headquarters in Chicago. The company expects to break ground this summer and occupy it by mid-2023. The R&D facility is expected to support development of the company’s iconic global snacks and treats brands.

The International Monetary Fund (IMF), Washington, D.C., in its flagship annual World Economic Report announced last week that global economic growth will slow significantly this year following the effects of the Russian invasion of Ukraine, rising inflation and interest rates and continuing effects of the COVID-19 pandemic (particularly in China). The IMF now forecasts the world economy to grow 3.6% in 2022, down from the 6.1% growth it forecast in October 2021. The new forecast is down 0.8% from the IMF’s projection in January. The IMF also forecast global growth for 2023 to be 3.6%, down 0.2% from its January forecast. The IMF attributes these downgrades primarily to the Russia-Ukraine war with its economic costs spreading through higher food and energy prices and disruptions in global trade. The IMF predicts that Ukraine’s economy will contract by 35% in 2022 and even if ended soon, the war will severely impede Ukraine’s economic activity for many years to come. Similarly, the IMF report forecasts Russia economy to shrink by 8.5% in 2022 and 2.3% in 2023, due primarily to reductions in energy exports to Western Europe and trade and financial sanctions by Western countries, along with the withdrawal of foreign businesses from various Russian industries. Other European economies are also shrinking due to the war’s effects. The IMF also reduced China’s economic growth from 5.6% forecast in October to just 4.4% now — much of this reduction is due to increased coronavirus infections. With reduced economic growth, R&D investments are similarly expected to shrink, although not as severely and not in aerospace and defense industries. Indeed, Lockheed-Martin, Bethesda, Maryland, had discussions last week with U.S. military executives about increasing production of weapons destined for Ukraine.

RDW Index member IBM, Armonk, New York, announced last week a stronger than expected 8% revenue increase in the first quarter based on continued improvements in its hybrid cloud platform. Revenues rose to $14.2 billion in Q1 from $13.2 billion a year earlier. Much of this was attributed to a 14% revenue increase in IBM’s hybrid cloud.

Rivian Automotive, Irvine, California, warned last week that the auto industry could soon face a shortage of battery supplies for electric vehicles (EVs). This challenge could surpass the effects of the current computer chip shortages, according to Rivian CEO RJ Scaringe. All the world’s current battery cell production is much less than 10% of what will be needed in 10 years, he says. Most of that expected supply chain does not currently exist.

In similar news to the Rivian item above, a report in the Wall Street Journal last week expects that even EV-leader Tesla, Austin, Texas, is being affected by current economic disruptions, such as inflation and declining economic growth. Tesla is modifying its long-term strategic plans to minimize the development of low-cost EVs and maximize the development of higher cost robotaxis to offset the effects of inflation.

Eight St. Louis research institutions announced last week that they are collaborating to create the Taylor Geospatial Institute. The member institutions (all based in and around St. Louis) include the Donald Danforth Plant Science Center, Harris-Stowe State University, Missouri University of Science & Technology, Saint Louis University, University of Illinois at Urbana-Champaign, University of Missouri-Columbia, University of Missouri-St. Louis and Washington University. These member institutions will fund research and development programs to draw top scientists in geospatial research to the St. Louis area. The institute will hire research staff, house cutting-edge scientific equipment and computing power and build an extensive data library to further attract top researchers in the geospatial field. The institute will initially be located at Saint Louis University. The National Geospatial Intelligence Agency (NGA) — a Department of Defense agency — has two locations in the St. Louis area, a $1.7 billion site in north St. Louis and one in Arnold Missouri, south of St. Louis. NGA is one of the U.S.’s “Big Five” intelligence gatherers (along with the CIA, National Security Agency, National Reconnaissance Office and the Defense Intelligence Agency. The new research collaborative said it plans to target food security, geospatial science and computation, health care and national security.

R&D World’s R&D Index is a weekly stock market summary of the top international companies involved in R&D. The top 25 industrial R&D spenders in 2019 were selected based on the latest listings from Schonfeld & Associates’ June 2020 R&D Ratios & Budgets. These 25 companies include pharmaceutical (10 companies), automotive (6 companies) and ICT (9 companies) who invested a cumulative total of nearly 260 billion dollars in R&D in 2019, or approximately 10% of all the R&D spent in the world by government, industries and academia combined, according to R&D World’s 2021 Global R&D Funding Forecast. The stock prices used in the R&D World Index are tabulated from NASDAQ, NYSE, and OTC common stock prices for the companies selected at the close of stock trading business on the Friday preceding the online publication of the R&D World Index.

Tell Us What You Think!