By Tim Studt, Contributing Editor

By Tim Studt, Contributing Editor

For 62 years, R&D World and its predecessors have published an annual R&D funding forecast. These reports predict the combined dollar amount of R&D investments expected by industry, government and academia for the upcoming calendar year. Over those years, the publications these reports have appeared in have changed their ownership and names several times.

The first forecast was published in the inaugural issue of Industrial Research in January 1959. For the next 40 years, these reports had a U.S.-only focus, due to the U.S.’s dominance in this arena. A growing international R&D presence then resulted in these reports covering all global R&D activities beginning with the September 2005 issue of R&D Magazine. The initial January 1959 report discussed how $12 billion would be spent on R&D in U.S. industry, government and academia. In this, our 62nd iteration of that continuing report, R&D World editors discuss how more than $2.4 trillion will be invested in 2021 in R&D industries, government labs and academic research centers across more than 115 countries.

Over the past six decades, R&D investments have declined several times because of economic variations and cycles. Often when industrial investments declined year-over-year, government R&D investments rose to such a degree that total R&D changed negligibly (and vice versa when industrial spending declined). This made for slow and steady increases over much of this period. During the Great Recession of 2009, global industrial and government R&D spending both dropped substantially. To offset this mostly rare economic event, the U.S. federal government passed emergency legislation under the American Recovery and Reinvestment Act (ARRA), which pumped more than $18 billion into R&D budgets (much of it spread out over several years). Similar recovery packages were passed in other countries during the same period.

Over the past year, the world economies have struggled with the effects of the COVID-19-based pandemic. Workers are quarantined, research materials and supplies are delayed, transportation systems have been crippled, production lines are slowed and interpersonal relations have been severely modified. The whole character of work (conventional and research-based alike) has seen dramatic operational changes. Rapid, globally-based vaccine research programs began in early 2020 with approved vaccines becoming available in mid-December. With these unprecedented research programs, a substantial number of inoculations will take place by June 2021 for possibly as much as 50% of the U.S. population.

Pandemic-effecting change

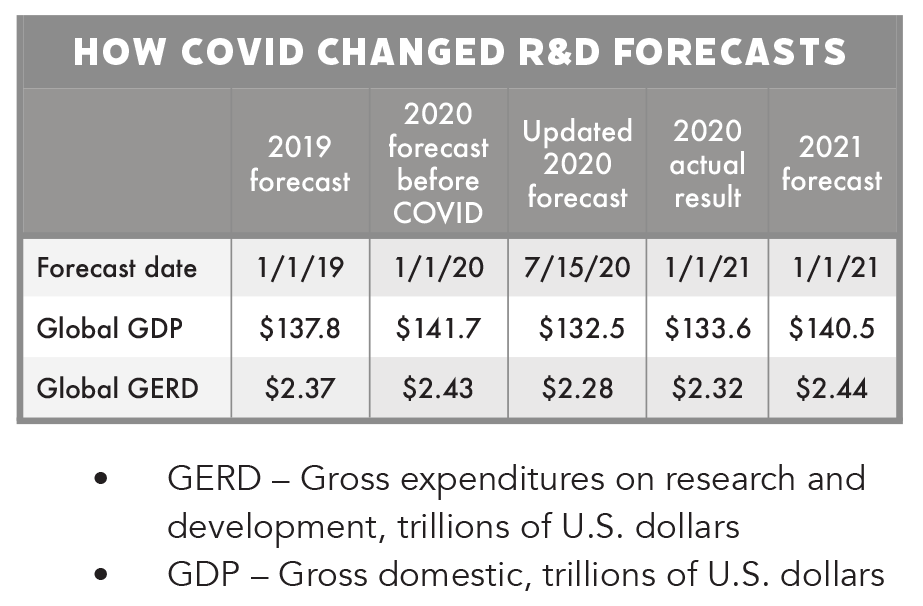

Last year’s 2020 Global R&D Funding Forecast was completed a couple of months before the COVID-19 pandemic became globally pervasive. When the pandemic spread throughout the world in the spring of 2020, and quarantines hit every aspect of global societies, R&D World editors updated the 2020 R&D Funding Forecast, which was published in August 2020. Details are as follows:

As noted, the global R&D forecast changed dramatically during 2020, as the most dire economic predictions made early in the year failed to materialize. At least part of this change was the result of proven and implemented vaccines in numerous countries near the end of the 2020.

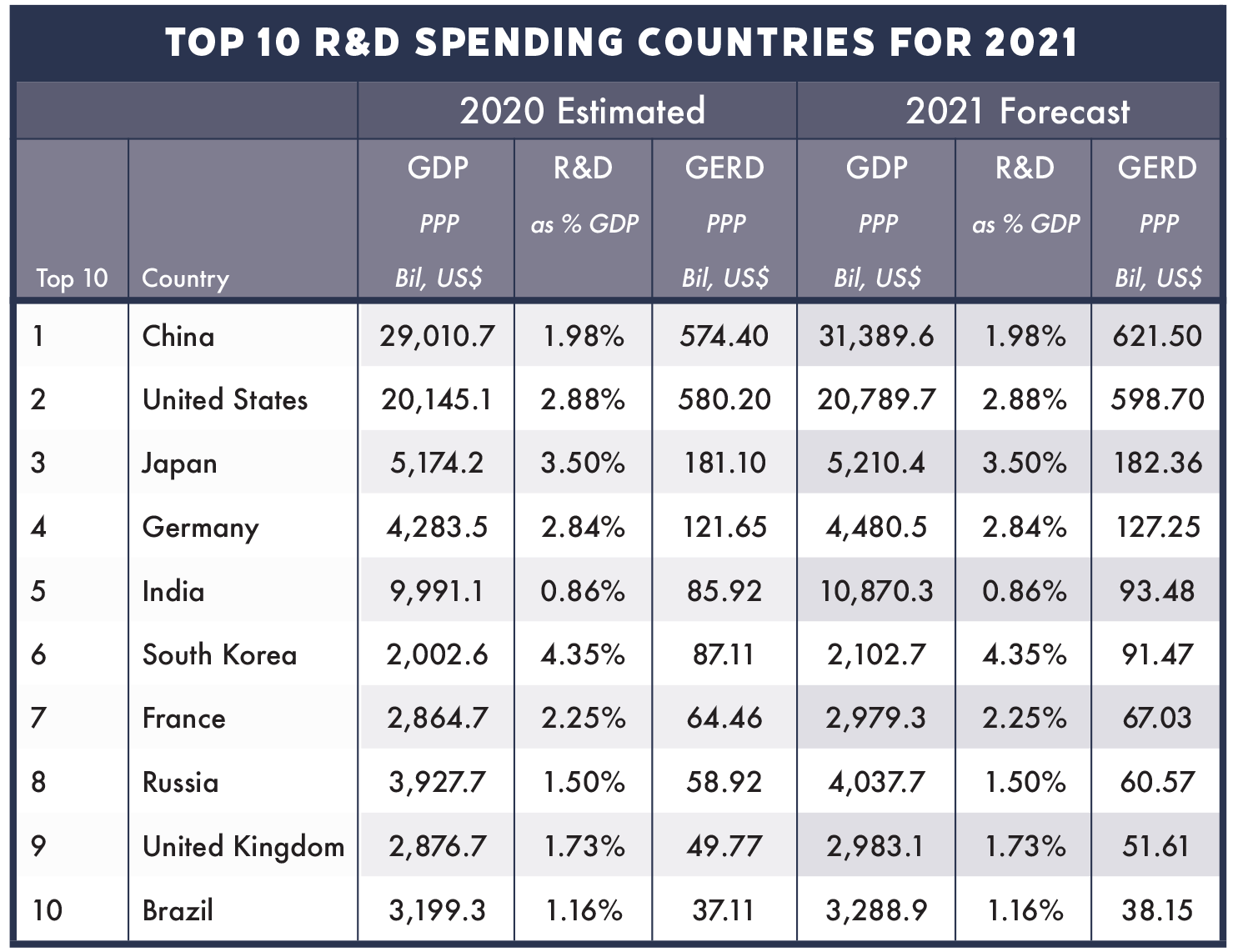

Our global R&D forecasts are strongly based on the individual economies of countries. This influence obviously varies, especially in the presence of a pandemic. The country GERD forecasts also are based on historic economic distributions for R&D. For example, China has for more than 20 years consistently invested heavily in its R&D. As a result, though its economic growth was hampered because of the pandemic (as was the case in all other countries), its historic investment of roughly 10% annual increases resulted in a rise in R&D for 2020. Almost all other countries (including the U.S.) saw their 2020 R&D investments decline from what they invested in 2019.

The continuing large annual increases in Chinese R&D investments (non-stop for more than 20 years) and the inability of the U.S. to match those increases results in a forecast of China outspending the U.S. (for the very first time) in R&D ($622 billion for China vs $599 billion for the U.S.) in 2021. This nearly 4% difference can be partially explained by a 2% improvement in China’s annual GDP compared to a 4% decline in U.S. annual GDP for 2020.

We’ve discussed this “passing of the torch” in R&D spending leadership for some time, but we felt it wouldn’t happen until 2022 at the earliest. The pandemic just moved that crossover point up a year or two. The gap between China and U.S. R&D investment is expected to widen over the next several years, assuming that future R&D investments maintain similar relationships.

Continuing regional disparities

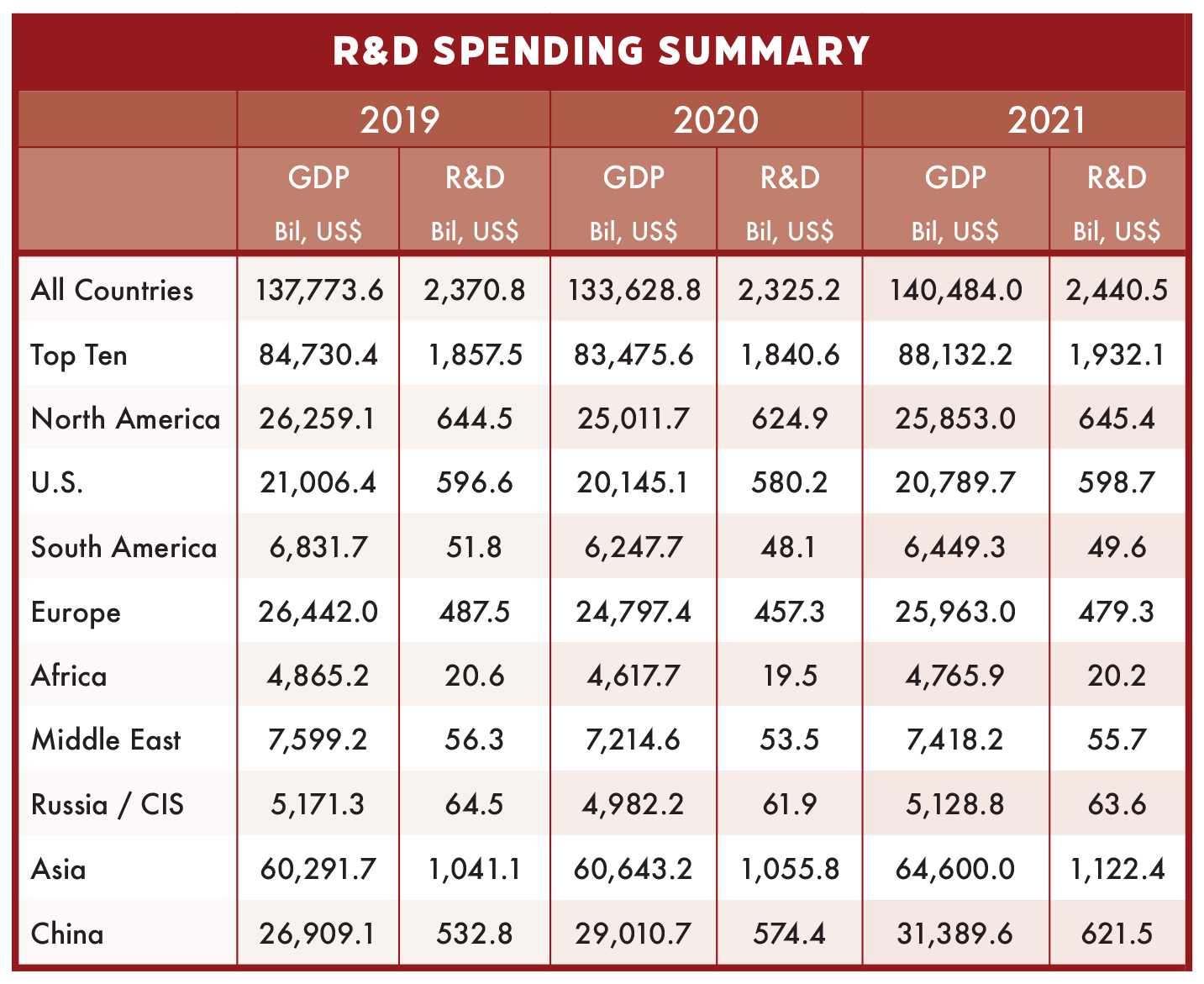

The geographic areas of greatest R&D investment have evolved over time, and this evolution will continue in 2021. The pandemic-effecting economic changes have not changed these “swings.” If anything, the pandemic actually accelerated the rate of these changes. North America, South America and Europe will continue to lose R&D leadership shares in 2021, even as their spending levels rise with the global economic recovery. Similarly, Asia, and China in particular, will see their share of worldwide R&D improve in 2021, along with even more dramatic improvements in R&D spending. China, Japan, India and South Korea will drive Asia’s global R&D spending share to 46% in 2021, along with an increase of more than $4 trillion in combined GDP.

While China will outpace the U.S. in R&D spending in 2021, India is expected to outspend South Korea and move up one spot in the top spender standings from #6 to #5. India has had a larger GDP than South Korea for many years (by a factor of over four), due primarily to its larger population (by a factor of 25+), but its R&D investment strategies have lagged behind most other major countries. Only within the past several years have we seen substantive improvements in India’s R&D investment policies.

Africa, South America and the Middle East regions will continue to languish in the hierarchy of R&D spenders. The combined total R&D investments of these three regions is just 5% of the total global R&D spending, despite creating more than 13% of the total global GDP. These ratios have not changed significantly over the past 10 years with no evidence for any meaningful improvements over the next five years.

This article is part of R&D World’s annual Global Funding Forecast (Executive Edition). This report has been published annually for more than six decades. The Executive Edition will be published in the April 2021 print issue of R&D World. To purchase the full, comprehensive report, which is 54 pages in length, please visit the 2021 Global Funding Forecast homepage.

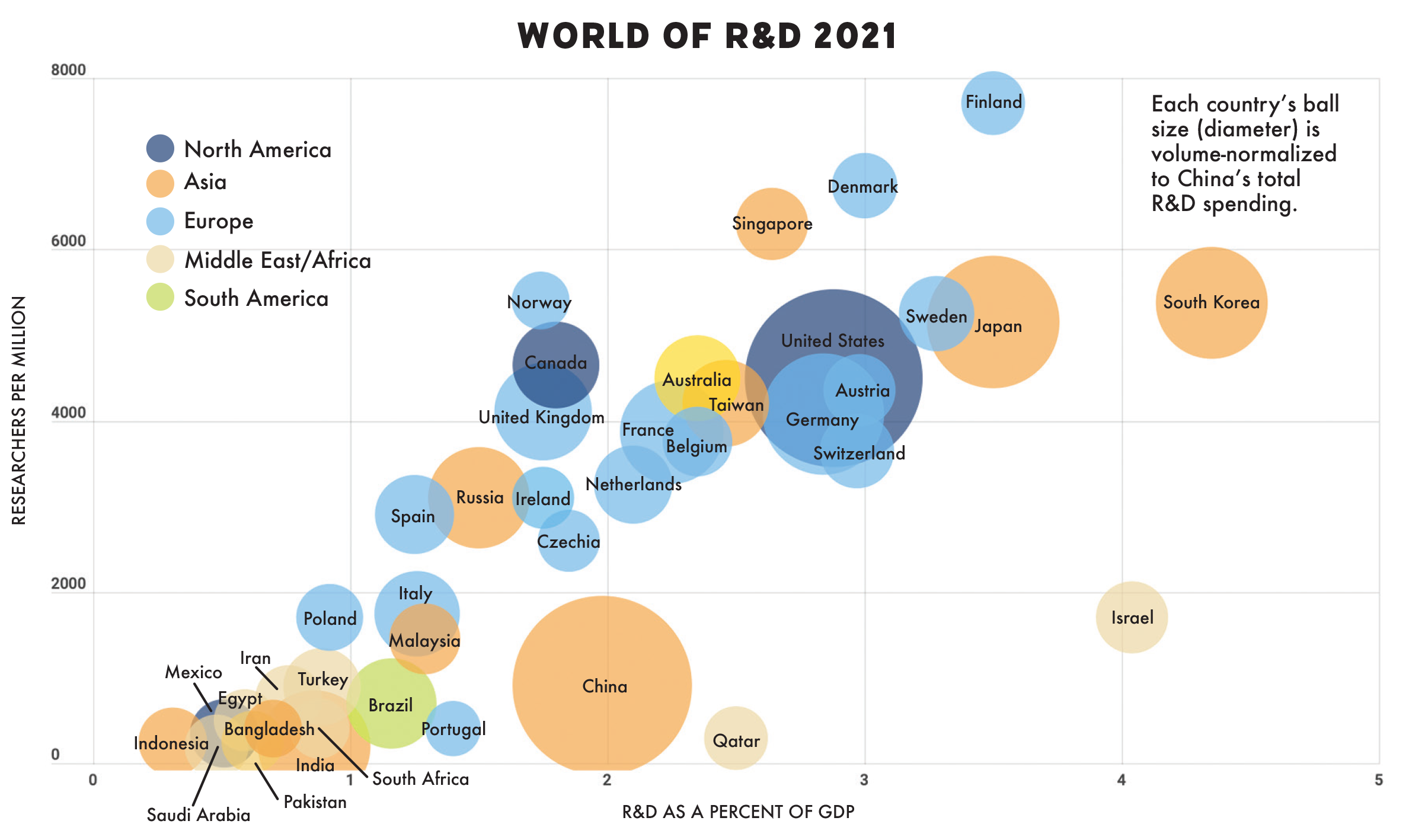

what is means Researchers per Milion