The United States leads the world’s nations in R&D performance with a global share of 28%. As that number continues to rise, the federal government is doubling down to ensure R&D in the U.S. is here to stay.

Ibrahim, CEO, Neo.Tax

While a recent tax change negatively impacts U.S.-based businesses that invest in R&D, it further penalizes companies that pursue these activities outside of the U.S.

Now, companies that depend on other nations for R&D will be left with a hefty tax bill — even if they are not yet profitable. With penalties for foreign activities expected to rise even further, it’s clear that this is not sustainable and that most companies will need to reconsider their R&D strategy.

The background

Incentivizing R&D through tax credits has been a long-standing practice in the United States, as businesses have been encouraged to invest in research and development to spur innovation and economic growth. The Tax Cuts and Jobs Act of 2017 (TJCA) brought significant changes to how companies can account for R&D expenses, which has caused some concerns among businesses that rely on R&D for their growth.

The TCJA now requires that companies capitalize and amortize their R&D expenses over five years for domestic R&D and over 15 years for foreign R&D for expenses incurred in tax years beginning after December 31, 2021. This means that the immediate benefit of the R&D tax credit has been reduced and severely penalizes companies with foreign R&D initiatives.

The TCJA now requires that companies capitalize and amortize their R&D expenses over five years for domestic R&D and over 15 years for foreign R&D for expenses incurred in tax years beginning after December 31, 2021. This means that the immediate benefit of the R&D tax credit has been reduced and severely penalizes companies with foreign R&D initiatives.

These changes represent an effort to modernize and simplify U.S. tax law, while also ensuring that businesses accurately reflect the costs associated with R&D activities in their financial statements. However, the new tax guidelines are forcing companies to rethink their R&D strategy.

On one hand, businesses with U.S.-based R&D have access to a highly skilled workforce, a large and diverse capital, and tax incentives that can help offset the costs of their R&D activities. On the other hand, R&D in the U.S. can be expensive, with high salaries, real estate costs, and regulatory compliance costs.

Incentivizing U.S.-based R&D through larger tax credits

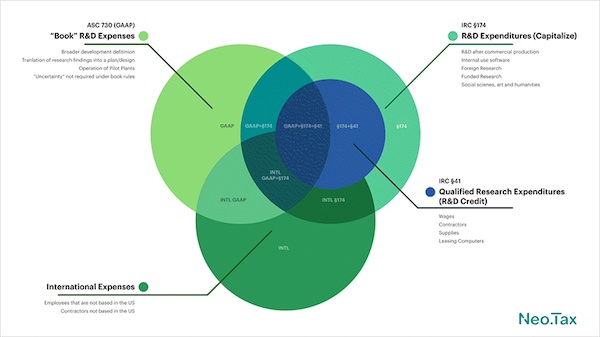

The TCJA brought about changes to Section 174 of the law, one of which requires that R&D expenses and software development costs must be capitalized and amortized.

The TCJA also modified Section 41, which pertains to the research credit. Specifically, the definition of “qualified research” now includes research that meets the criteria for “specified research or experimental expenditures,” as defined under Section 174.

After identifying qualified research expenses and determining additional costs needed, businesses must determine the appropriate method by which to monitor the amortization of the capitalized expenses. Lastly, businesses need to document their effort to identify and quantify R&D expenses for future reference and adjust based on their needs.

Why this is happening

Prior to the TCJA, companies could choose to either immediately deduct R&D expenses or capitalize and amortize them over time.

By requiring companies to capitalize on R&D expenses, the U.S. government aims to improve the accuracy and consistency of financial reporting as well as align U.S. tax law with international accounting standards. This change may also make it easier for businesses to comply with tax rules, as they will no longer have to make a choice between immediate expensing and capitalization.

Overall, the R&D capitalization requirements under the TCJA represent an effort to modernize and simplify U.S. tax law, while also ensuring that businesses accurately reflect the costs associated with R&D activities in their financial statements.

Another perspective: Some believe that the changes to R&D capitalization under TCJA were a budgeting trick for the U.S. government to pass the bill. According to this view, for the TCJA to pass through Congress, it needed to be approved by the congressional budget committee. Since there were several tax cuts in the bill, the government needed to add a provision to show that it would be making money by increasing taxes over time by allowing for short-term tax benefits.

Another perspective: Some believe that the changes to R&D capitalization under TCJA were a budgeting trick for the U.S. government to pass the bill. According to this view, for the TCJA to pass through Congress, it needed to be approved by the congressional budget committee. Since there were several tax cuts in the bill, the government needed to add a provision to show that it would be making money by increasing taxes over time by allowing for short-term tax benefits.

Regardless of the motive behind the R&D capitalization changes, the TCJA has faced significant criticism and has been a topic of debate during its passage. Some believed that the law would be repealed due to its perceived shortcomings and the way it was passed. However, the TCJA remains in effect, and businesses continue to navigate the changes introduced by the law.

Moving R&D to the U.S.: The pros

There are several benefits that companies can reap by moving their R&D initiatives to the U.S.:

- Access to a talented workforce. The U.S. has a highly skilled workforce with expertise in diverse fields. This provides businesses with access to talented researchers and engineers who can help drive innovation.

- Strong intellectual property protection. The U.S. has strong intellectual property laws and regulations that protect companies’ proprietary technologies; this is crucial for companies investing in R&D.

- Access to capital. The U.S. has a large and diverse pool of investors, including venture capital firms and angel investors, who can provide funding for R&D efforts.

- Tax incentives. The U.S. government offers tax incentives, such as the R&D tax credit, which can help offset the costs of R&D activities.

- Access to world-class research facilities. World-class research facilities and universities in the U.S. provide businesses with access to cutting-edge technology and resources.

Moving R&D to the U.S.: The cons

While there are benefits to businesses for moving their R&D to the U.S., there are also some drawbacks:

- High costs. R&D in the U.S. can be expensive, with high salaries, real estate, and regulatory compliance costs.

- Competition for talent. There is intense competition for talent in the U.S. which can make it difficult for businesses to attract and retain top talent.

- Regulatory burden. The U.S. has a complex regulatory environment, which can be a significant burden for companies investing in R&D, especially in such highly regulated industries as healthcare and biotechnology.

- R&D capitalization. The TCJA requires companies to capitalize and amortize R&D expenses and software development costs over five years for U.S.-based and fifteen years for R&D based overseas, which can increase the administrative burden and decrease the immediate tax benefits of R&D.

How businesses can mitigate the financial impact of the TCJA

Act now. The process can be time-consuming and requires careful consideration. Start early to identify, analyze, and quantify R&D expenses to ensure a smooth process. This is particularly important for taxpayers who do not claim tax credits for R&D activities.

Build on what they have. When computing a federal research credit under Section 41, taxpayers should start by identifying qualified research expenses (QRE), which overlap with R&D expenses. They should then determine additional costs needed for purposes outlined in Section 174, like employee benefits, qualifying contractor costs, foreign research expenses, and indirect costs. It is important to note that some wages in QREs may not be related to development activities.

Be intentional. To decide if R&D expenses can be capitalized and amortized, taxpayers should analyze the direct and indirect costs associated with resolving uncertainties or developing software in a given tax year. It’s important to take a thoughtful approach to assess the advantages and disadvantages of capitalization and amortization and to see if changes to operations or business structure can reduce their impact.

Execute and track process. After identifying and quantifying Section 174 costs, taxpayers must determine the appropriate method to monitor the amortization of the capitalized expenses. Taxpayers should document their effort to identify and quantify R&D expenses for future reference. This includes process insights, identifying information sources, and understanding cost categorization and tracking.

Plan ahead. Analyzing R&D costs may reveal opportunities for structural and operational changes that can improve future processes, enhance benefits, or mitigate detriments. Taxpayers should act based on this knowledge when it aligns with other business needs.

Will penalties for offshore R&D increase?

Given the recent emphasis on bringing more R&D activities onshore in the U.S., it is likely that there will be more penalties on companies that choose to offshore them.

The TCJA mandates that companies with foreign R&D operations must capitalize and amortize their R&D costs over a period of 15 years, and foreign R&D expenditures cannot be used to offset these costs in claiming the R&D tax credit.

Additionally, proposals have been made to change the tax code in ways that would make it more expensive for companies to offshore R&D, including eliminating certain tax deductions or imposing new taxes on offshore profits. For example, some lawmakers have proposed a minimum tax on foreign earnings that would make it more expensive for companies to shift profits to low-tax countries.

Finally, there has been increased scrutiny of companies that offshore their R&D, particularly if it leads to job losses or reduced economic growth in the U.S. Government agencies and industry groups have called for increased transparency and reporting requirements to ensure that companies are not taking advantage of tax loopholes or other incentives to avoid paying their fair share of taxes.

Are these guidelines here to stay?

Various legislative proposals have been introduced in Congress to repeal or modify the R&D capitalization requirements under the TCJA since its enactment in 2017.

In December 2019, the Research and Development Tax Credit Expansion Act was introduced in the Senate. The bill proposed to extend and enhance the R&D tax credit, and it also aimed to repeal the R&D capitalization requirement under the TCJA. However, this bill did not make it to the floor for a vote.

In December 2019, the Research and Development Tax Credit Expansion Act was introduced in the Senate. The bill proposed to extend and enhance the R&D tax credit, and it also aimed to repeal the R&D capitalization requirement under the TCJA. However, this bill did not make it to the floor for a vote.

In March 2020, the House of Representatives introduced the Research Investment to Spark the Economy (RISE) Act, which aimed to repeal the R&D amortization requirements under the TCJA. The bill did not pass.

In May 2021, the Senate introduced the Innovation Promotion Act of 2021, which would have modified the R&D capitalization requirements by allowing small businesses to expense up to $250,000 of R&D costs annually. It also would have extended the amortization period to 10 years for larger businesses. The bill did not pass.

As of April 2022, there have been no significant actions taken to repeal the R&D capitalization requirements under the TCJA. However, there have been ongoing discussions among policymakers and industry groups about the potential impacts of the requirements on innovation and economic growth.

Today, there appears to be consensus in Congress to modify the R&D credit legislation. Earlier this year, Senators Maggie Hassan and Todd Young recently proposed the American Innovation and Jobs Act, which seeks to expand and make permanent the R&D tax credit while also increasing the tax credit rate for certain small businesses. The bill also proposes to repeal the R&D capitalization requirements imposed by the TJCA, making it easier for companies to immediately expense their R&D costs.

In addition to these legislative efforts, there have been various industry groups and advocacy organizations that have called for the repeal of the R&D capitalization requirements, arguing that it places an undue burden on businesses and discourages innovation.

However, the law still exists, and companies must take steps to mitigate the financial impact of the changes. Companies should start early and be intentional when identifying, analyzing, and quantifying R&D expenses to ensure a smooth process, especially for those who don’t claim tax credits.

The bottom line

The changes brought by the TCJA in the accounting of R&D expenses have a significant impact on how companies will do business going forward. With an inevitable impact on those who rely on foreign activities, businesses must learn to adapt to these guidelines. While there’s no one-size-fits-all approach, preparing early and taking action will help to minimize the financial burden of the TCJA.