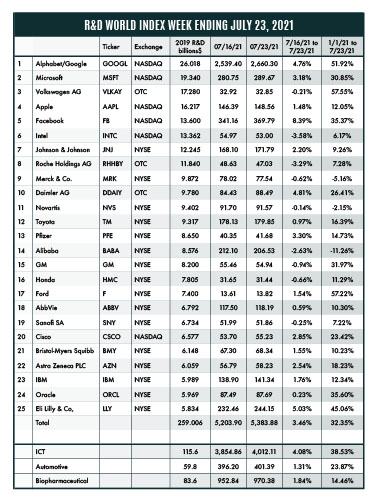

The R&D World Index (RDWI) for the week ending July 23, 2021 closed at 5,383.88 for the 25 companies in the R&D World Index. The Index was up 3.46% (or 179.98 basis points) from the week ending July 16, 2021. The stock of 16 R&D World Index members gained value from 0.23% (Oracle) to 8.39% (Facebook). The stock of nine R&D World Index members lost value from -0.14% (Novartis) to -3.58% (Intel).

Click to enlarge.

Biotech firm Regeneron Pharmaceuticals has announced plans for a six-year, $1.8 billion expansion at its Tarrytown, N.Y., headquarters site. The plans include R&D buildings, preclinical production and associated support facilities. Along with this expansion, the company plans to add 1,000 staff personnel over the next five years. The 900,000 ft2 expansion will include up to eight buildings, three parking garages and a central utility plant. Regeneron developed a successful COVID-19 antibody cocktail, REGEN-COV in 2020. The company is expected to receive up to $100 million in tax credits from the New York state government.

RDW Index member Intel announced last week that the current global semiconductor shortage could stretch into 2023. Automaker Volkswagen, already struck by chip shortages, also warned last week that the shortage could worsen over the next six months and will last well into 2022. Intel stated that it takes a long time to build manufacturing capacity, but that the current shortages will ease up for automakers by the end of the year. Intel has earlier announced the nearly $25 billion in construction of multiple new chip manufacturing facilities in Arizona and New Mexico.

Prices of electric vehicle (EV) battery materials have skyrocketed in 2021 forcing automakers to secure key materials. Prices of lithium carbonate, used in battery cathodes, have doubled over the past twelve months, according to research firm Benchmark Mineral Intelligence last week. Prices for cobalt hydroxide, which boosts energy density and battery life, have also risen by more than 40% over the past year. The lithium market is expected to fall into deficit in 2022, according to the research firm. EV automakers Tesla, BMW and GM have all signed long-term deals with materials suppliers. Chinese EV automakers are likely to benefit from these deals since they dominate the processing of the materials that go into the manufacture of EV batteries.

Mercedes-Benz AG joined other automakers last week in their announcement to go all electric by 2030. The Daimler RDW Index member stated that it plans to invest more than $47 billion between 2022 and 2030 to reshape its business around EV products. All new Mercedes vehicles produced after 2025 will be EV only. Internal combustion vehicles will still be available for purchase as long as there is consumer demand, according to the company. Eight Mercedes EV models will be manufactured at seven locations on three continents starting in 2022. The company also has collaborated with Royal Dutch Shell to create more than 30,000 charge points in Europe, China and North America by 2025. The company has also acquired UK-based electric motor company Yasa to help integrate its manufacturing and development. Mercedes also will reduce its investments in combustion engines and hybrid technologies by 80% between 2019 and 2026.

Dubai Electricity and Water Authority (DEWA) announced last week that it formed a collaboration with Stanford University to develop an advanced system to forecast photovoltaic (PV) panel production. DEWA used its Space-D program at its large Al Maktoum solar park (forecast for 5,000 MW by 2030) using its (Stanford-codeveloped) Independent Power Producer model. The new system reduces errors in the forecast to less than 10%. The system utilizes artificial intelligence, deep learning and high-density cameras on satellites to predict irradiance and dust and cloud movement. Dubai wants 75% of its total power capacity to be obtained from clean energy sources by 2050.

Idat-Oberstein, Germany-based BioNTech, the co-developer of Pfizer’s COVID-19 vaccine, announced last week that it plans to buy a cell therapy R&D platform and clinical manufacturing plant in Gaithersburg, Md., from Gilead Science’s Kite Pharma. BioNTech will use the Kite plant to bolster supply for its U.S. clinical trials. BioNTech plans to make additional investments and increase headcount over the current 50 Kite headcount, although no details were disclosed. BioNTech expects to see $15 billion in revenues in 2021 from the COVID-19 vaccine.

The semiconductor chip shortage seen in the auto industry is now starting to affect cell phone manufacturers, according to various analysts. Cell phone makers generally purchase key parts about six months in advance, but those stockpiles are now starting to dwindle. Samsung, Google, China’s Xiaomi have all either raised prices, cut shipments and/or reduced revenue forecasts due to chip shortages. Apple’s cell phones and Samsung’s premium cell phone models avoided these actions due to their “supply-chain clout”. The most critical chips are power-management devices, display drivers, applications processors and 4G and 5G chipsets. The overall industry has seen nearly a 20% drop in sales in the first half of 2021 compared to that in 2020, according to Counterpoint Research.

The UK government’s new R&D People and Culture Strategy announced last week is aiming to make the UK “the most ideal place for research and innovation by 2035.” The UK made several commitments to make this happen including: 1) developing a New Deal for post-graduate research students starting in 2021; 2) providing support for flexible, cross-sector training programs to encourage more movement and collaboration; and 3) creating a Good Practice Exchange to develop, test and evaluate ways to ensure the right culture is created within academia. The UK has also created a Global Talent Visa and Scale-up visa routes to attract top research talent to the UK.

The U.S. is using its extensive market pressure to prevent Netherlands-based ASML Holdings from creating an export license allowing it to ship its extreme ultraviolet lithography system to China. The $150 million, 180-ton systems are used to make state-of-the-art computer and cellular equipment by such companies as Intel, Samsung, Apple and Taiwan Semiconductor Manufacturing Co. The Biden administration has asked for this restriction on national security grounds. China wants the system for its Huawei Technologies Co. The restriction has led to increased conflicts between the U.S., the Netherlands and China. ASML competitors, including Canon and Nikon, only make older-generation ship fabrication tools. China is considered about 10 years away from creating its own competitive system.

R&D World’s R&D Index is a weekly stock market summary of the top international companies involved in R&D. The top 25 industrial R&D spenders in 2019 were selected based on the latest listings from Schonfeld & Associates’ June 2020 R&D Ratios & Budgets. These 25 companies include pharmaceutical (10 companies), automotive (6 companies) and ICT (9 companies) who invested a cumulative total of nearly 260 billion dollars in R&D in 2019, or approximately 10% of all the R&D spent in the world by government, industries and academia combined, according to R&D World’s 2021 Global R&D Funding Forecast. The stock prices used in the R&D World Index are tabulated from NASDAQ. NYSE, and OTC common stock prices for the companies selected at the close of stock trading business on the Friday preceding the online publication of the R&D World Index.

Tell Us What You Think!