The intensity of the chip race is written in the patent data. Between early 2024 and late 2025, Qualcomm added nearly 6,000 active patent families to its portfolio, a 25% jump that makes it the S&P 100’s single biggest gainer in absolute terms. Rival Nvidia expanded its own IP moat by 21% over the same period. For R&D leaders, that part of the story is familiar but the scale is notable.

The surprise in IFI CLAIMS’ latest S&P 100 ranking is where the fastest patent growth is coming from. Banks, insurers, retailers and coffee chains now look, on paper, like some of the most aggressive technology companies in the index. JPMorgan Chase, Bank of America, and Capital One are stacking patent families around machine learning and digital payments. UnitedHealth is filing on AI driven question answering. Nike and Starbucks are building portfolios around digital goods and smart, connected equipment.

The center of gravity in S&P 100 patents still sits in chips and cloud, yet the list of companies that behave like platform technology firms is widening. Viewed alongside global World Intellectual Property Organization (WIPO) data, the picture is a tight link between where the patent boom is happening and where durable R&D moats are forming.

In recent WIPO data, Asia’s patent offices shoulder roughly 70% of the world’s application volume, with China’s office alone handling close to half of global filings. Computer technology is now the single largest field. That is the macro view. IFI CLAIMS’ new S&P 100 ranking lets us zoom in on who actually holds the patent “moats” inside the 100 most valuable U.S. companies, and how those moats are shifting. The analysis draws on IFI’s snapshot of active patent families as of November 3, 2025.

Long-term investors look for economic moats that protect a company’s competitive edge. Of the 100 most valuable companies in the U.S., 99 of them have one thing in common: patents. — IFI Claims

What “active patent families” tell us

IFI’s S&P 100 ranking looks at active patent families grouped by ultimate owner rather than annual grants. In patent practice, a family represents one invention and the related filings in multiple jurisdictions. IFI defines a patent family as “a single invention and its collection of patents filed worldwide to protect it,” and counts only those families that remain in force. Once protection ends, the market opens to competitors.

On that measure, the S&P 100 together control roughly 524,000 active patent families, down slightly from about 530,000 in early 2024, with almost half of that IP concentrated in just ten companies. In a market where intangible assets account for an estimated 90 percent of S&P value, those active families say more about real moats than any single year grant count. For R&D and IP teams, they indicate where companies are continuing to pay to maintain live protection, not simply where they experimented with filings in one busy year.

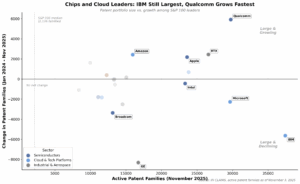

Chips and cloud at the core: IBM still leads, Qualcomm takes the growth crown

The top of IFI’s S&P 100 table looks familiar. IBM still holds the largest active patent estate in the index, with about 37,400 families, even after shedding more than 5,600 since early 2024 as it prunes older patents and concentrates around AI, hybrid cloud, and quantum technologies. Qualcomm is the clear climber. It now owns almost 29,800 active families, adding nearly 6,000 in less than two years, more than any other company in the ranking. Apple, Amazon, and Nvidia all expand their portfolios by double digit percentages, while Microsoft and several other long time leaders modestly shrink their active holdings.

This pattern matches global application data. The chip and cloud companies that have filed heavily over the past decade also dominate active portfolios. At the same time, some older industrial players and telecom operators are letting more patents drop than they add. For engineering leaders inside those sectors, that erosion signals where internal R&D bets are being trimmed and where future bargaining power may shift toward chip and cloud suppliers with dense, carefully maintained estates.