[Adobe]

The relative decrease in uncertainty following the presidential election is, of course, a factor. “Organizations understand at least who is going to be in power in Washington,” Lyons said. “But I think the second thing is the economy has seemed to stabiliz in terms of inflation and economic uncertainty.” This steadier footing enables firms to invest in essential data infrastructure, leverage cloud collaborations (e.g., the Cancer AI Alliance), and deploy Gen AI to tackle complex, data-intensive processes such as clinical trials and pharmacovigilance.

Executive outlook 2025

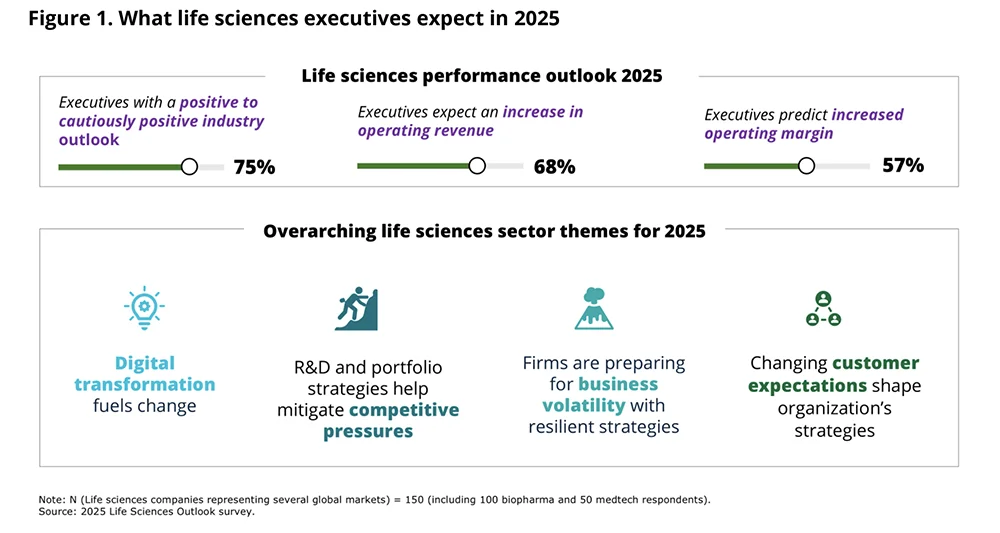

- 75% of global life sciences executives are optimistic about 2025

- 68% anticipate revenue increases

- 57% predict margin expansions

—Deloitte: ‘2025 life sciences outlook’

Across the value chain, organizations are leaning into digital transformation. Nearly 60% of surveyed leaders plan to boost generative AI (Gen AI) investments, moving beyond pilot projects to integrate AI-driven insights into day-to-day processes. Biopharma leaders anticipate that AI could drive up to an 11% increase in value relative to revenue over the next five years, while medtech firms foresee up to a 12% reduction in total costs within two to three years. At the same time, 56% of executives are prioritizing real-world evidence (RWE) and multi-modal data strategies—crucial steps toward improving R&D productivity and mitigating the decades-long downward trend noted by “Eroom’s law.”

[From Deloitte’s ‘2025 life sciences outlook’]

Pete Lyons

While optimism prevails, leaders remain aware of ongoing headwinds. Pricing and access to medicines are top concerns, along with shifting regulatory frameworks—including the Inflation Reduction Act in the U.S. and evolving clinical trial regulations in Europe—that demand agile strategies. Mergers and acquisitions are expected to rise, helping companies fill pipeline gaps and bolster innovation portfolios. Drawing on data from 150 C-suite executives across the United States, Europe, and Asia, the Deloitte survey highlights an industry at a crossroads: incremental stability is encouraging but the industry continues to confront formidable R&D hurdles. Yet executives are also poised to translate digital investments and data-driven insights into sustainable growth. In this environment, the capacity to harness Gen AI, fortify data ecosystems, and strategically manage regulatory and market uncertainties will set leaders apart as they navigate a pivotal year ahead.

Generative AI adoption continues to be a focus area

Yes, genAI has been hyped, but the technology continues to make its presences felt in the healthcare ecosystem. “I’ve seen many emerging technologies over my career, but none have gained traction as fast as Gen AI,” said Lyons. Implementation challenges, however, persist as well. The survey reveals a significant scaling gap, with only 11% of organizations achieving enterprise-wide deployment. Organizations are following a structured implementation pathway, beginning with process efficiency optimization—applying Gen AI to streamline document preparation, streamline pharmacovigilance workflows, and accelerate clinical development cycles. “As models ingest more data and learn, efficiency and effectiveness improve,” Lyons explained. These advanced implementations focus on multimodal data analysis, integrating clinical, genomic, and imaging datasets to mine new R&D findings.

AI’s financial impact

Biopharma companies could generate up to 11% value relative to revenue through AI investments over 5 years, while medtech firms may achieve up to 12% cost savings within 2-3 years.

—Deloitte: ‘2025 life sciences outlook’

Establishing the technical backbone for growth in 2025 demands more than just adopting new tools—it requires a strategic approach to data governance and prioritization. “Data readiness is key—if you don’t have clean, accessible data, the technology won’t deliver the full benefit,” Lyons said. This point resonates with insights from Takeda’s Corporate Strategy Officer & CEO Chief of Staff, Akiko Amakawa, who underscored the importance of developing a framework to prioritize digital investments “just like we have been managing our R&D pipeline.” According to Amakawa, who was quoted in the Delotte report, digital initiatives span a spectrum of objectives—risk management, operational efficiency, customer satisfaction—that defy a single ROI metric. To address this complexity, organizations are building robust data ecosystems and standardized infrastructures, ensuring that the foundation is in place before layering on advanced analytics and AI-driven applications on top. Such strategic planning and alignment can help life sciences organizations fully tap Gen AI’s transformative potential in the coming years.

Aiming to reverse R&D productivity declines

R&D productivity, which has trended downward over the past decade, may benefit significantly from Gen AI and better data management. By applying advanced analytics and AI models to complex tasks, companies can trim cycle times and costs while uncovering new insights that might inform more effective drug discovery efforts. According to Lyons, “Pharmacovigilance or clinical trial processes involve massive amounts of data, and these models need time and input to become more accurate and reliable.” Cloud adoption plays a core role here, as pharma has been relatively proactive in migrating to cloud platforms compared to other healthcare sectors. Data standardization, secure access, and collaborative alliances can help organizations centralize and validate their data, thereby enabling more effective use of Gen AI and advanced analytics. Efforts like the Cancer AI Alliance—pooling data and expertise across industry and academic stakeholders—aim to break down innovation barriers and bolster both efficiency and effectiveness in R&D.

Patent cliff challenge

The biopharma industry faces potential loss of over $300 billion in sales through 2030 due to patent expirations, with 77% of executives expecting increased M&A activity in 2025.

—Deloitte: ‘2025 life sciences outlook’

The looming patent cliff, which could jeopardize $300 billion in revenues by 2030, intensifies the pressure on companies to fill pipelines and refresh their portfolios. This urgency, combined with reduced R&D productivity, has contributed to pharma stocks lagging behind the broader market. M&A activity has historically been a strategic lever to address innovation gaps and mitigate the impact of patent expirations, and the trend is likely to continue as companies seek to bolster their pipelines and strengthen their competitive positions.

Shifting regulatory sands

Regulatory shifts add another layer of complexity. Drug pricing pressures, underscored by the Inflation Reduction Act, remain front-and-center issues and will likely continue as a bipartisan focus areas. Evolving FDA processes, changes in clinical trial regulations, and legal uncertainties stemming from the post-Chevron landscape mean that life sciences organizations must continuously adapt. The Supreme Court’s decision in Loper Bright Enterprises v. Raimondo, which rescinds the Chevron Doctrine’s longstanding deference to agency expertise, suggests future regulations may face heightened judicial scrutiny. Without the buffer of agency discretion, life sciences firms may need to anticipate more legal challenges and invest in stronger compliance infrastructures, rigorous data validation protocols, and traceable AI/ML implementations.

Beyond pricing and regulation, life sciences companies are also reassessing supply chain resilience in the face of geopolitical uncertainty. “Geopolitical uncertainty is prompting companies to think about resilience and redundancy in their supply chains,” notes Lyons. Building redundancy and ensuring continuity—rather than simply onshoring goods across the board—can help mitigate risks such as climate events disrupting critical inputs. As Lyons emphasizes, the focus is on “creating a more resilient global supply chain in a complex, interconnected world.’ Cybersecurity concerns also loom, as increasingly digital and data-driven operations require robust protections against evolving threats.

GLP-1s a continued bright spot

Meanwhile, the GLP-1 market signals a return to primary-care-oriented blockbusters after years focused on specialty and oncology products. Companies are exploring competing therapies, various formulations, and a range of potential applications beyond diabetes and obesity, with metabolic health at the core of emerging innovations. Durability of effect, patient adherence, and long-term outcomes remain open questions.

Added to that, shifting authority structures, data-driven compliance requirements, and heightened technical infrastructure needs underscore the imperative for a proactive, adaptive approach. As one executive observed in the Deloitte report, “Drug pricing remains front and center. The Inflation Reduction Act is having real effects, potentially influencing R&D strategy.”

In this more fluid regulatory environment, companies that invest in agile regulatory intelligence, data maturity frameworks, and risk-based approaches to compliance stand the best chance of thriving. By anticipating legal shifts, strengthening data readiness, and focusing AI-driven efforts on the most critical processes, life sciences organizations can navigate the complexities of the coming year—and beyond—with confidence and strategic foresight.

Beyond pricing, regulation, and supply chain resiliency, the industry’s search for new growth avenues underscores a return to broader therapeutic categories. Nowhere is this more evident than in the burgeoning GLP-1 market, which is ushering in a resurgence of primary-care-focused blockbusters after an era dominated by niche, specialty, and oncology products. Although the market is now consolidated, competition in the metabolic market is growing fierce. Biopharma companies are “developing competing therapies, looking at different formulations, administration methods, and dosing regimens,” Lyons noted. As companies race to develop next-generation therapies and explore indications beyond diabetes and obesity, GLP-1s exemplify the expansive opportunities—and challenges—ahead. Durability of treatment effects, patient adherence, and long-term outcomes remain pressing questions, but the sheer market potential speaks volumes about the direction of life sciences innovation. JP Morgan estimates that the market could exceed $100 billion annually by 2030. “GLP-1s represent a return to a primary-care-oriented blockbuster model, after years of focusing on specialty, rare, and oncology products. There’s a tremendous market opportunity, potentially hundreds of billions of dollars,” said Lyons.