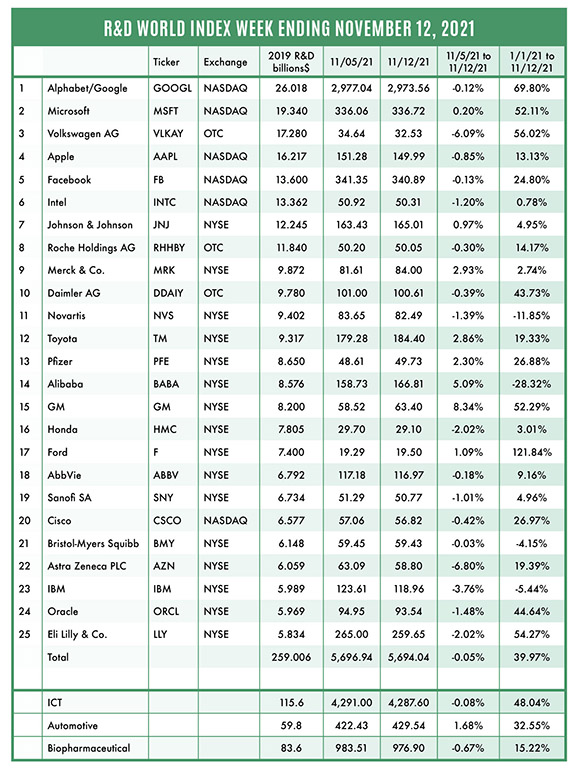

The R&D World Index (RDWI) for the week ending November 12, 2021, closed at 5,694.04 for the 25 companies in the RDWI. The Index was down -0.05% (or -2.90 basis points) from the week ending November 5, 2021. The stock of eight RDWI members gained value from 0.20% (Microsoft) to 8.34% (General Motors). The stock of 17 RDWI members lost value from -0.03% (Bristol-Myers Squibb) to -6.80% (Astra Zeneca PLC).

Click to enlarge.

Three large global corporate entities — General Electric, Johnson & Johnson and Toshiba — with a combined annual R&D investment of more than $17 billion announced last week that they were splitting up their organizations into multiple independent companies. The three companies will focus on aviation, healthcare and power. GE is a major supplier of large aircraft engines (developed and manufactured at its Lafayette, Ind. site); a global leader in MRI systems (developed and manufactured at its Waukesha, Wis. site); and a major supplier and integrator of power systems for renewable energy systems. The multinational GE conglomerate currently employs 205,000 and had $75.6 billion in revenue in 2020, down from $224 billion in 2004. GE is incorporated in New York with headquarters in Boston. The company has two major Global R&D locations — its more than 100-year-old corporate site in Niskayuna, N.Y., near Schenectady and its 20-year-old-facility in Bangalore, India. No mention was made in the GE announcement concerning details of its future R&D plans. Individual GE manufacturing and development sites often have some of their own R&D capabilities on site.

RDW Index member Johnson & Johnson, New Brunswick, N.J., also looked at its organization and decided they could get stronger growth by separating into smaller individual units focused on their core competencies. J&J announced last week that they would split off their 1) $15 billion annual revenue consumer products division (which sells BandAid bandages, Tylenol, baby powder and more) and 2) their high-margin pharmaceutical drug and medical device business. Each of these businesses require different corporate skill sets and the separation will allow the company to focus specific resources on each. Again, no details on R&D plans for each of the two divisions was provided and likely won’t be known for some time. J&J’s R&D spending for 2020 was expected to be about $12.3 billion and close to $12.5 billion for 2021. Each J&J new division would still be among the world’s largest in its specific field. J&J’s reorganization follows similar moves by competitors Merck and Pfizer over the past several years.

Toshiba, Tokyo, announced last week that it planned to split into three different companies by March 2024 to follow a path similar to that of GE and for similar reasons. The three new companies will focus on 1) infrastructure, 2) electronic devices and 3) flash memory, including Toshiba’s stake in Kioxia Holdings Corp. Over the past several years, Toshiba has sold off divisions focused on medical devices, personal computers, consumer electronics and its U.S. nuclear power unit Westinghouse Electric, which declared bankruptcy in 2017. This new move by Toshiba was likely accelerated by its 2015 accounting scandal which resulted in foreign ownership of more than half the company. Toshiba’s R&D investments have been declining as a result of its sell-off of its high-tech divisions and is expected to be $1.5 billion in 2021, down from $1.7 billion in 2019.

The U.S. Department of Labor reported last week that the U.S. consumer price index (CPI, an indicator of inflation rates) rose to a 30-year high of 6.2% from the same time in 2020. This was the fastest 12-month rate increase since 1990 and the fifth consecutive month of inflation above 5%. The core price index, which excludes food and energy, rose to 4.6% in October, which beat September’s 4.0% gain and the largest increase since 1991. Price increases covered a broad range of goods, except for airline fares and alcohol. These latest statistics reveal that the Federal Reserve may be more likely now to raise interest rates. The Fed has indicated that they will reduce their monthly bond purchases and may end them completely by June 2022. The Fed will stop buying bonds before raising interest rates, according to analysts.

The United Kingdom (U.K.) announced last week that it has backed a $546 million Rolls-Royce funding round to develop the country’s first small nuclear reactor. These small modular reactors (SMRs) are planned to be manufactured in factories with parts small enough to be transported on trucks and barges and assembled faster than large scale conventional nuclear reactors. Each SMR is planned to power about one million homes. The plans also state that the R&D and production of these reactors could create up to 40,000 new jobs and be exportable. Nuclear reactors currently provide about 20% of the UK’s electricity, but all but one are scheduled to close by 2030. New SMRs would not be available until the early 2030s and will need extensive approval by the UK’s Office for Nuclear Regulation.

RDW Index member AstraZeneca, Cambridge, U.K., announced last week that it has launched a new R&D division focused on vaccines. AstraZeneca’s collaboration with Oxford University has resulted in a COVID-19 vaccine that is being supplied to low to middle-income countries at cost, according to the company. It has supplied the largest share for COVAX (38%), which is backed by the United Nations (U.N.). Due to initial issues concerning a very rare occurrence of blood clots associated with the AstraZeneca vaccine, the U.S. Food and Drug Administration (FDA) has not yet approved the vaccine, even though some U.S.-manufactured products have been exported to other countries.

A large 2.8 million foot2 R&D-focused development spread across seven buildings was proposed last week for South San Francisco. The buildings would range in size from three to seven stories with appropriate infrastructure changes identified in the proposal. An environmental impact report needs to be created prior to project approval and initial evaluations cite considerable concerns during the building phase of the project.

The Biden administration plans to update an existing Trump-administration R&D plan targeted at combatting orbital debris. The new plan would include an interagency group within the National Science and Technology Council that deals with national security and space issues. The plan is scheduled to be released in 2022 and will build off the Trump R&D plan released in January 2021. Agencies involved in creating the report include NASA, the Department of Defense, the Federal Communications Commission (FCC), National Oceanic and Atmospheric Agency (NOAA), the Federal Aviation Administration (FAA) and the U.S. Space Force (which will be the lead agency).

R&D World’s R&D Index is a weekly stock market summary of the top international companies involved in R&D. The top 25 industrial R&D spenders in 2019 were selected based on the latest listings from Schonfeld & Associates’ June 2020 R&D Ratios & Budgets. These 25 companies include pharmaceutical (10 companies), automotive (six companies) and ICT (nine companies) who invested a cumulative total of nearly 260 billion dollars in R&D in 2019, or approximately 10% of all the R&D spent in the world by government, industries and academia combined, according to R&D World’s 2021 Global R&D Funding Forecast. The stock prices used in the R&D World Index are tabulated from NASDAQ, NYSE and OTC common stock prices for the companies selected at the close of stock trading business on the Friday preceding the online publication of the R&D World Index.

I find this trend to be enormously problematic, if not ominous. We live in a world where investment for growth in segmented markets will work against the very kinds of interdependent, inter-systemic functionality that the world needs to make the most efficient use of scarce resources. Climate change is mandating a fundamental reorganization of the world’s economic premises, methods and values. This splitting up of enterprises into “core competency” R&D and market segments is exactly the opposite of what is needed to achieve a new generation of end-to-end design synergies through system-of-systems engineering and strategic planning. It is a harbinger of yet another round of disjoionted incrementalism, justified as the best strategy for “growth,” when traditional growth itself is what will increasingly dismantle anything resembling progress, as capital “grows” cancerlike, consuming its human and natural inputs.