After the trade conflict dramatically escalated on April 9, new U.S. tariffs pushed cumulative rates on many Chinese goods toward 104%. Separate “reciprocal” tariffs targeting the EU and other trading partners were set to follow.

Beijing swiftly responded, announcing retaliatory tariffs against the U.S. would jump to 84%, effective April 10. The EU, meanwhile, prepared its own countermeasures. The rapid-fire escalation sent markets into turmoil.

But in a sudden pivot late on April 9, the U.S. imposed a 90-day pause on reciprocal tariffs for most trading partners, including the EU. This temporary rollback reverted rates to a recently established baseline of 10%, allowing breathing room for negotiations.

China, notably, was left out of this reprieve. Tariffs on Chinese goods were instead ratcheted higher, reportedly reaching between 125% and 145%.

The abrupt shifts deepened economic fears. JPMorgan Chase CEO Jamie Dimon, who previously warned tariffs could dampen growth and spike inflation, declared a recession was now “probably” a “likely outcome.” Trump-supporting billionaire investor Bill Ackman painted an even starker picture, warning of an “economic nuclear winter” without a negotiation pause.

But what might the impact of all of this be on R&D spending?

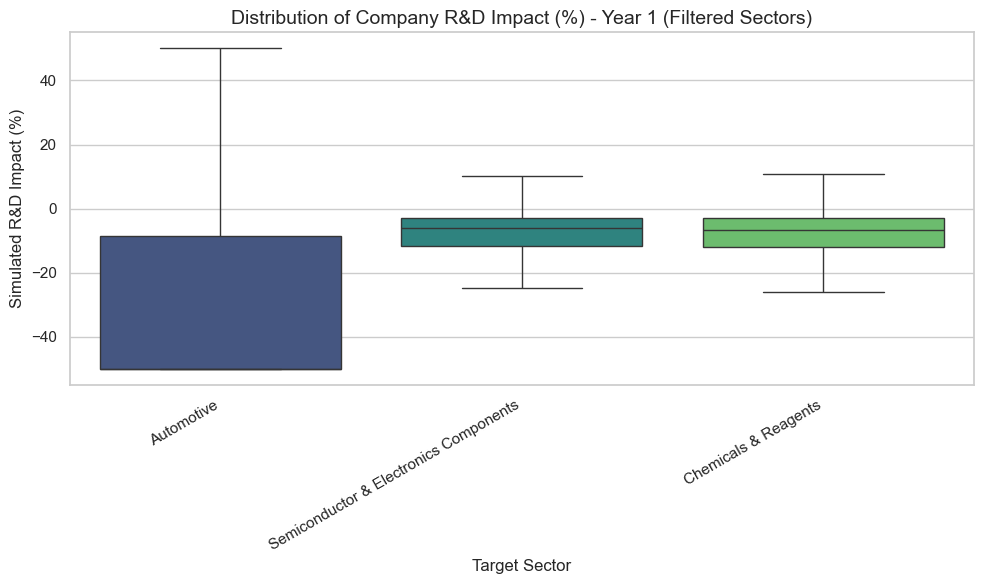

Our Monte Carlo simulation, analyzing the potential impact over five years under policy uncertainty, reveals that the proposed tariff escalations could significantly curtail R&D investment across key U.S. sectors, though with highly uneven effects. The model shows dramatic differences in vulnerability between industries: while some face negligible direct impacts within the model, others could see R&D investment plummet by over a third in the first year.

Model limitation note: This simulation explores specific tariff channels based on economic assumptions. It does not predict the future and omits real-world complexities such as individual firm strategy, detailed operations, and macro effects. Its projections are thus estimates under defined assumptions.

Automotive could see some of the steepest cuts

A rendering of a VW R&D facility in China. The company cut 35,000 workers in late 2024 while targeting $1.7 billion in savings. Meanwhile, Volkswagen’s Audi said it would cut up to 7500 workers in Germany by 2029.

The simulation projects the automotive sector could see the biggest drops in R&D spending — potentially a steep 38% average decline in the first year. This significant projected impact stems directly from the sector’s acute exposure to both import and export tariff pressures. The simulation models the consequences of policies like the 25% tariff on imported automobiles and key parts (engines, transmissions, electrical components) that President Trump invoked in March 2025 under Section 232, as a White House Fact Sheet notes. Our model captures how these tariffs sharply increase input costs for manufacturers deeply integrated into global supply chains. Simultaneously, retaliatory tariffs imposed by trading partners on U.S. vehicle exports diminish foreign sales profitability, hitting the sector’s bottom line from another angle. The potential magnitude of this dual pressure is underscored by market concerns, with analysts warning tariffs “could decimate company earnings” (See: CNBC) and estimates projecting consumer price hikes of up to $6,000 per vehicle (See: Reuters, citing Cox Automotive).

Compounding these direct tariff impacts are broader industry headwinds that further pressure profitability and, consequently, the capacity for sustained R&D investment. Persistent supply chain instability, exacerbated by geopolitical tensions and trade friction, continues to squeeze margins. Furthermore, the sector is navigating a challenging transition to electric vehicles (EVs). J.D. Power points to stagnating EV market share growth, with S&P Global Mobility revising long-term EV sales forecasts downward. Affordability issues and infrastructure gaps likely increase hesitancy around major, future-focused R&D spending in electrification. Finally, Oxford Economics points to higher interest rates as a persistent factor, though they could potentially ease slightly from peaks.

Semiconductor could see double-digit R&D drop in an escalated trade conflict case

[Image courtesy of Adobe Stock]

Yet, significant storm clouds are gathering that temper this optimism and pressure investment decisions. Industry analysts explicitly flag trade tariffs alongside geopolitical risks and global economic policy uncertainty as key challenges. Compounding this is the uncertainty surrounding the very programs designed to bolster domestic production; President Trump has openly called the CHIPS and Science Act a “horrible, horrible thing” and suggested Congress should “get rid of” it. That would potentially halt or claw back billions in promised subsidies crucial for funding capital-intensive fab construction. This policy instability adds risk to the massive capital commitments required for modern manufacturing and supply chain diversification, even as firms grapple with high costs and persistent talent shortages.

The market’s sensitivity to trade friction is evident. For instance, NVIDIA, despite strong earnings and a record 2024, saw significant stock volatility in early 2025. This uneven performance partly resulted from investor jitters surrounding tariff announcements and their potential impact on the AI boom. Meanwhile, industry giants like Intel are navigating severe internal pressures. The firm, which has a new CEO, is undertaking major restructuring and layoffs amid recent revenue struggles.

Chemicals and reagents could face more moderate R&D headwinds

A novel ORNL microscope captured an image of lily pollen, which is colorized to show the distribution of two molecular groups. The instrument quickly shows chemical details. Credit: Uvinduni Premadasa/ORNL, U.S. Dept. of Energy

The simulation suggests a noticeable but less severe impact on the chemicals and reagents sector, with R&D spending potentially decreasing by an average of around 7.15% in the first year. This reflects the sector’s position experiencing pressures from both import costs and export retaliation, though likely moderated compared to the automotive industry.

As a diverse sector providing essential inputs across the economy, chemical manufacturers are exposed to tariffs on imported precursor materials, driving up production costs, as Chemical & Engineering News has observed. Simultaneously, U.S. chemical exports often face retaliatory tariffs in key markets (See: Society of Chemical Industry), squeezing profitability on foreign sales. Our model captures these dual pressures. The projected impact is less extreme than in the auto sector, potentially due to several factors averaged across this broad industry: the specific mix of products facing tariffs, varying demand elasticities across different chemical types (likely less sensitive overall than vehicles but more so than essential medicines), and the specific destinations of exports relative to retaliatory measures. Furthermore, the health of major downstream markets like construction and consumer goods, themselves affected by trade policy and economic conditions, as Tax Foundation has noted, adds another layer of indirect pressure influencing investment capacity.

Thus, the 7.15% projected R&D decline represents a potentially tangible drag from trade friction across a wide range of chemical producers, reflecting genuine cost and revenue pressures identified by industry analyses, even if not reaching the critical levels seen in sectors with more concentrated tariff exposure like automotive.

Pharma could see more of a tariff cushion

The simulation projects a relatively minimal or negligible direct impact (0.0%) on R&D spending specifically for the pharma sector, leading to its omission in the final graphs. While not implying that the industry is immune to trade disruptions, economists have traditionally found the pharma sector to have low price elasticity. This contrasts sharply with sectors like automotive where demand is more price-sensitive.

Consequently, retaliatory tariffs raising prices in export markets did not lead to a significant drop in quantity demanded in the model, meaning the model calculates minimal profit loss from reduced export revenue. In addition, R&D spending is less discretionary in the biopharma landscape. That is, the nature of drug development itself may somewhat insulate R&D budgets from short-term profit fluctuations compared to other industries. Unlike deferring a vehicle model refresh, halting mandatory, multi-year clinical trials owing to temporary margin pressure effectively eliminates a drug candidate’s entire potential future revenue stream. This essential, binary nature of trial progression makes core R&D spending less cyclically adjustable and could thus provide a sort of cushion to R&D spending in the sector.

That said, the model’s finding of limited direct tariff impact doesn’t shield pharmaceutical R&D from significant headwinds. Regulatory uncertainty looms large, driven by the Inflation Reduction Act’s drug pricing rules, the law’s potential repeal, and staffing reductions at key agencies like the FDA. Even in late 2024, industry surveys reflected this anxiety, with executives citing regulatory and geopolitical risks as top concerns, as Deloitte noted. Additionally, operational pressures like persistently high development costs and talent shortages add to the complexity. Investor caution is also evident: declining valuation multiples since 2018 highlight skepticism about future profitability. Taken together, these factors could independently constrain R&D spending as the biopharma sector looks to limit risk.

Summary of the Monte Carlo results based on 1000 runs projecting out one year. Note: For the automotive sector, the long upper whisker (which incidentally is not an error bar) indicates a very wide spread or high variance in the simulated results for individual companies within the sector at year 1. While the median is negative, the whisker extending up to +50% means that even though the typical simulated impact is negative, there were simulated outcomes for some companies in the sector where the R&D impact was significantly positive, reaching the upper limit imposed by the plotting code’s clipping.

Methodology note

The current economic climate features unusually high unpredictability. Standard economic analysis often falls short in such conditions. For instance, static models struggle to capture the dynamic impact on long-term corporate strategy, especially for investments like R&D. Furthermore, significant uncertainty surrounds the tariffs themselves: Will they persist, be removed, or escalate further? Will implementation be broad or follow a patchwork approach?

To cut through this complexity, we employ a distinctive Monte Carlo simulation framework—an analytical engine designed specifically to navigate uncertainty. By running 1000 scenarios over a five-year horizon, our simulation explicitly models policy impermanence by factoring in the annual probability that tariffs might be reversed. This analysis is based on the full 1000 simulation runs; initial preliminary results based on 100 runs showed very similar outcomes, reinforcing the stability of these findings.

It also integrates real-world data on company financials, sector-specific trade exposure (using detailed import/export data), and tariff schedules. Data here was collected from USA Trade, the European Commission, and news releases (for tariff rates). The model also uses research-based economic parameters. Those included how R&D investment responds to profit changes, tariff pass-through rates, and exchange rate offsets.

Year 1 Impact Estimates (1000 Simulations)

The following table summarizes the Year 1 impact estimates derived from the full 1000 simulation runs. These figures correspond to the “Mean Impact (%)”, “Median Impact (%)”, “5th Pctle (%)”, and “95th Pctle (%)” columns in the analysis output.

| Target Sector | Mean Impact (%) | Median Impact (%) | 5th Pctle (%) | 95th Pctle (%) |

|---|---|---|---|---|

| Automotive | -38.13 | -38.13 | -38.15 | -38.11 |

| Semiconductor & Electronics Components | -12.00 | -12.17 | -12.92 | -10.86 |

| Chemicals & Reagents | -7.15 | -7.15 | -8.04 | -6.25 |

| Other | 0.00 | 0.00 | 0.00 | 0.00 |

| Pharmaceuticals | 0.00 | 0.00 | 0.00 | 0.00 |

| Software | 0.00 | 0.00 | 0.00 | 0.00 |

Recap on 100 vs. 1000 simulations

While running 100 Monte Carlo Simulations took under one hour, bumping it up to 1,000 took more than 50 hours of non-stop processing on an M4 Mac CPU. The results between the two were extremely similar.

Automotive: The figures were identical to two decimal places.

Semiconductors and chemicals: There were very minor shifts (less than 0.1 percentage points) in the mean, median, and percentile values.

Confidence: The main benefit of running 1000 simulations instead of 100, in this case, was to significantly increase the confidence that the observed impacts (especially the large one in automotive) are stable features of the model under the specified parameters and data, and not just artifacts of a smaller sample size.

References

- Amiti, M., Redding, S. J., & Weinstein, D. E. (2019). The impact of the 2018 tariffs on prices and welfare. Journal of Economic Perspectives, 33(4), 187-210. https://www.aeaweb.org/articles?id=10.1257/jep.33.4.187

- Caldara, D., Iacoviello, M., Molligo, P., Prestipino, A., & Raffo, A. (2020). The economic effects of trade policy uncertainty. Journal of Monetary Economics, 109, 38-59. https://doi.org/10.1016/j.jmoneco.2019.11.002 (Linked from ScienceDirect page)

- Cavallo, A., Gopinath, G., Neiman, B., & Tang, J. (2021). Tariff pass-through at the border and at the store: Evidence from US trade policy. American Economic Review: Insights, 3(1), 19-34. https://www.nber.org/papers/w26396 (Working Paper)

- Furceri, D., Hannan, S. A., Ostry, J. D., & Rose, A. K. (2022). Macroeconomic consequences of tariffs. IMF Economic Review, 70(1), 171-195. https://www.nber.org/papers/w27654 (Working Paper)

- Jeanne, O., & Son, S. K. (2024). To what extent are tariffs offset by exchange rates? Journal of International Money and Finance, Volume 144, 103089. https://doi.org/10.1016/j.jimonfin.2024.103015 (Published version, update from ‘forthcoming’)

- Peters, B., Roberts, M. J., Vuong, V. A., & Fryges, H. (2021). Firm R&D investment and export market exposure. Research Policy, 50(6), 104271. https://doi.org/10.1016/j.respol.2021.104271 (Linked from ScienceDirect page)