Each year, the top 2,500 or so international R&D spenders collectively invest more than $1 trillion in R&D. The roster of R&D heavyweights is shaping up to look broadly similar to prior years, but NVIDIA is poised to crack into the top 15 given its recent AI-driven growth. If anything, NVIDIA’s ascent into the ranks illustrates the dominance of hardware and software firms in R&D investment. However, in 2024, Intel had a broadly different trajectory, with the company reporting revenue declines in Q2 and Q3. The firm also announced a $10 billion cost-reduction plan, including a headcount reduction of over 15,000 employees, while CEO Pat Gelsinger exited abruptly in December 2024.

While stalwarts like Alphabet, Microsoft, and Apple maintain consistent, long-term investment patterns, the accelerated trajectory of firms like NVIDIA highlights how strategic bets in emerging AI-driven computing ecosystems along with a deeply entrenched hardware-software ecosystem—exemplified by CUDA’s widespread adoption and the high switching costs it imposes—can rapidly reshape competitive standings.

AI’s central role across top six

Alphabet’s self-driving Waymo vehicle

It’s telling that AI has emerged as a central focus for the likely top six R&D spenders—Alphabet, Microsoft, Apple, Huawei, Samsung Electronics, and Meta, which has, to a degree, pivoted away from its earlier metaverse emphasis toward AI. Alphabet is pushing AI infrastructure, genAI, and advanced computing at scale, while Microsoft is embedding AI into its enterprise and cloud ecosystems. Meanwhile, Apple is channeling R&D into AI-enabled custom silicon and on-device intelligence while implementing its Apple Intelligence suite across iOS and macOS. It features advanced capabilities like Image Playground for AI-powered image generation and ChatGPT integration with Siri for enhanced natural language processing. In addition, Huawei is tapping AI to enhance telecommunications and automotive technologies. Samsung Electronics has intensified its focus on AI semiconductor development, optimizing memory solutions for large language models, and expanding on-device AI capabilities in its consumer ecosystem.

Pharma: More R&D spending but not always more profits

Beyond this AI-centric core, other sectors reinforce the sense that high R&D spending is a strategic prerequisite, not a guarantee of outsized profit margins. Pharma leaders like Bristol-Myers Squibb, Roche, Merck, and Pfizer exemplify how sprawling R&D budgets drive long-term pipeline innovation rather than immediate returns. The industry has grappled with steadily increasing R&D costs over past decades without a corresponding increase in the number of new drug approvals. Yet, there is some reason for optimism. According to Deloitte’s 2025 Life Sciences Outlook, 68% of surveyed industry executives anticipate revenue increases despite ongoing cost pressures and patent cliffs. Some Big Pharma companies have faced recent challenges, however. In 2024, Pfizer implemented a $4 billion cost reduction strategy while appointing new scientific leadership. Meanwhile, Bristol-Myers Squibb’s $1.5 billion cost-cutting initiative, including significant workforce reductions, occurred alongside strategic acquisitions like Karuna Therapeutics to strengthen its neuroscience portfolio. Merck’s situation further aligns with these pressures, as the world’s biggest pharma (by revenue) worked to address the approaching patent expiration of Keytruda, which represents 40% of its revenue.

VW facing challenge in balancing R&D and profitability

[VW]

NVIDIA’s rise in the ranks

In tech, NVIDIA’s recent surge illustrates how an integrated approach—fusing proprietary software frameworks, specialized chips, and robust partner ecosystems—can catapult a company into the upper echelons of R&D spending. Meanwhile, Goldman Sachs’ analysis cautions that the vast investments fueling these AI projects, estimated at around $1 trillion, may take years to translate into substantial economic benefits. Companies may find themselves investing heavily in chip design, data centers, and energy infrastructure well before the full financial rewards are realized, the firm warned.

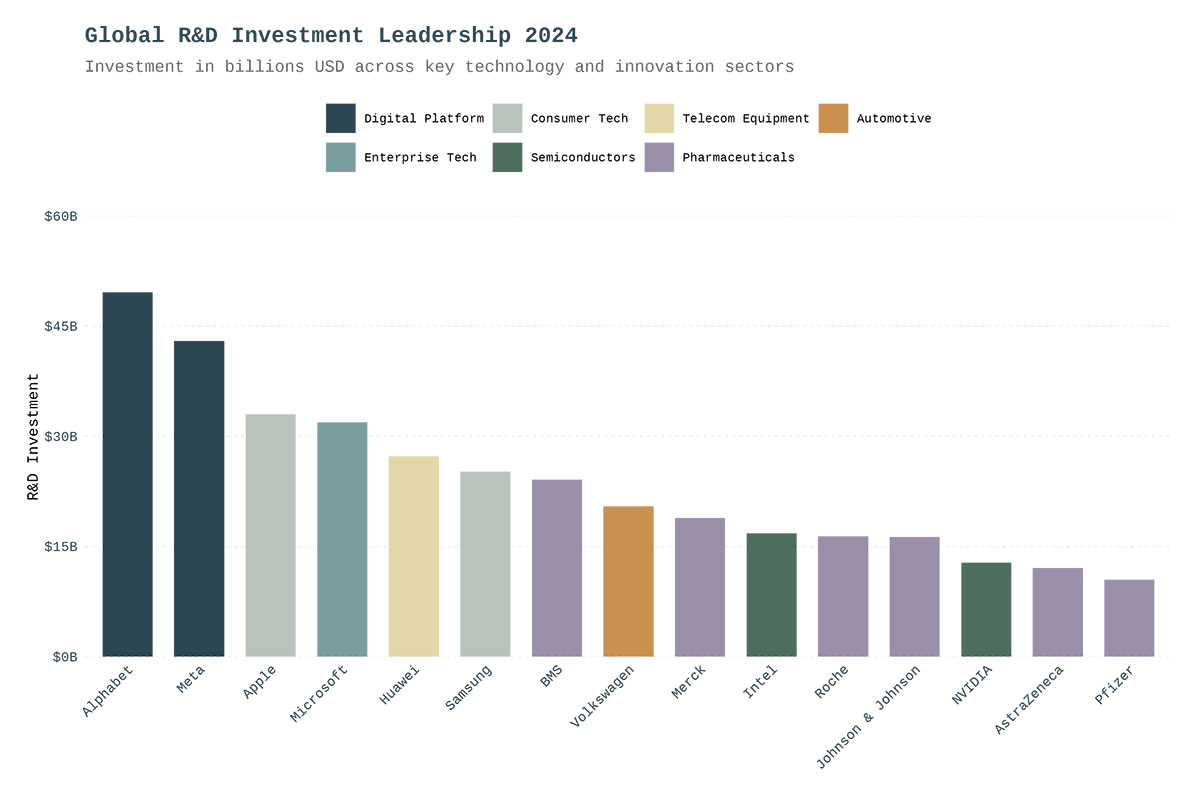

Top 15 projected R&D spenders of 2024

The table below highlights the top 15 projected R&D spenders for 2024, reflecting how these trends—sustained AI investment, intensifying competition in semiconductors, long-cycle pharmaceutical bets, and the reshuffling of legacy players—are shaping the global innovation landscape with Alphabet continuing to sitting on top of the list as it has since 2019, elbowing Samsung off its perch.

| Rank | Company | Projected 2024 R&D Investment (USD Billion) | Strategic Focus |

|---|---|---|---|

| 1 | Alphabet (Google) | ~49.6 | AI infrastructure, quantum computing, autonomous systems |

| 2 | Meta | ~43.0 | AI models, AR/VR, infrastructure for large language models |

| 3 | Apple | ~33.0 | Custom silicon, AR/VR platforms, AI integration |

| 4 | Microsoft | ~31.9 | AI integration, cloud infrastructure, enterprise tech |

| 5 | Huawei | ~27.3 | Telecommunications, smartphone & automotive tech |

| 6 | Samsung Electronics | ~25.2 | Semiconductors, displays, AI integration |

| 7 | Bristol-Myers Squibb (BMS) | ~24.1 | Biopharma pipeline expansion, immuno-oncology |

| 8 | Volkswagen (VW) | ~20.5 | Electric vehicles, autonomous driving, software integration |

| 9 | Merck | ~18.9 | Drug discovery, clinical trials, immunotherapies |

| 10 | Intel | ~16.8 | Advanced semiconductors, AI accelerators |

| 11 | Roche | ~16.4 | Oncology, personalized medicine, diagnostics |

| 12 | Johnson & Johnson | ~16.3 | Biopharma, medical devices, AI in healthcare |

| 13 | NVIDIA | ~12.8 | AI chips, data center platforms, software ecosystems |

| 14 | AstraZeneca | ~12.1 | Oncology, rare diseases, next-gen biologics |

| 15 | Pfizer | ~10.5 | Vaccines, antiviral drugs, inflammation & immunology |

Methodology

Where available, we used the most recently reported last twelve months (LTM) or full fiscal-year R&D expenditures. For companies that provided fiscal-year results (e.g., Apple, Microsoft, NVIDIA), we aligned to their respective fiscal end-dates and took the latest reported data, adjusting if necessary for Q4 estimates based on their run-rate. For calendar-year reporters, we used LTM data through Q3 2024 and then projected Q4 figures based on the average quarterly run-rate observed during the first three quarters. In the case of Huawei, we applied a reported year-to-date growth rate of 29.4% through Q3 2024 to its last known annual R&D base to approximate full-year 2024 spending. For NVIDIA, we considered FY2025 Q3 results and applied a similar spending trajectory into Q4. Huawei’s figure was derived by applying the known growth rate in revenue and maintaining its R&D intensity, as publicly reported. All euro-based figures were converted to U.S. dollars using an approximate EUR/USD exchange rate of 1.08–1.10, based on the average rates during the relevant periods. Amazon was not included in the ranking despite its significant R&D investment as the company does not break down research-related expenses as a line item.