A late-July U.S.-EU trade deal capped most EU imports, including pharmaceuticals, at 15%, easing fears of triple-digit levies and supporting a rebound in life-sciences tools shares. On July 23, Thermo Fisher raised the lower end of guidance and said the tariff situation was improving, reinforcing the risk-relief trade. Danaher and Agilent also have reported their outlook lifting as risk receded.

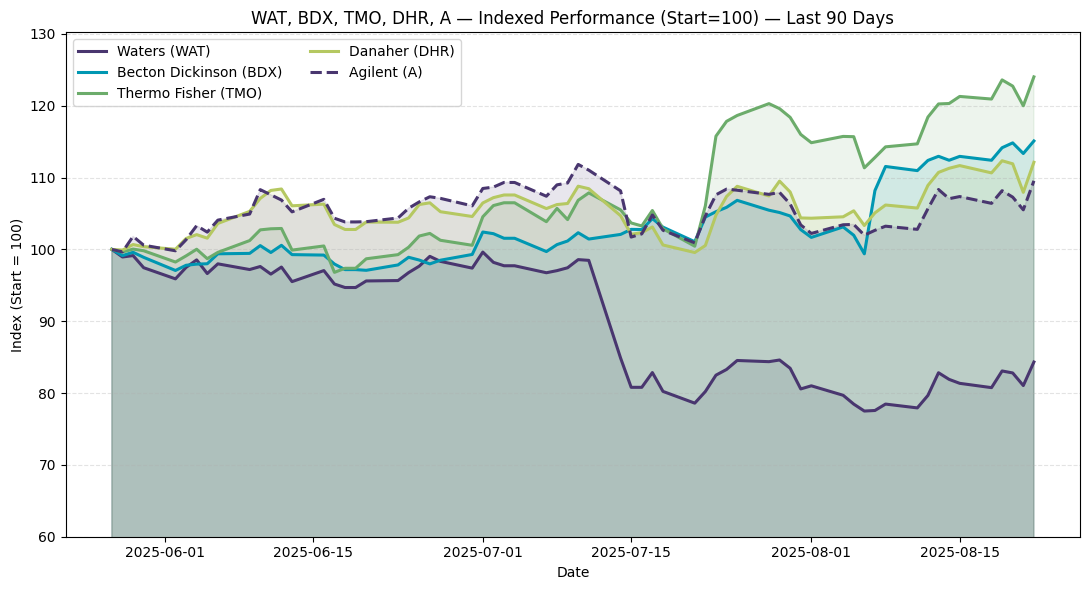

Waters is the exception. Its July 14 announcement to combine with BD’s Biosciences & Diagnostic Solutions unit via a $17.5 billion Reverse Morris Trust, shifting the portfolio toward regulated, high-volume diagnostics, left WAT down 14.4% versus July 11 closes, versus 3% to 15% gains for core peers through August 22. The tape implies a discount for integration complexity and higher leverage despite strategic logic. The shared graph of indexed performance over the last 90 days shows Waters (solid dark purple) trending sharply lower post-announcement, while peers like Thermo Fisher (green) climbed and others held flat.

Following the announcement, J.P. Morgan said the deal leaves value creation dependent on the successful integration and execution by Waters management. On August 4, Jefferies reiterated its buy rating with a target cut to $385 as analysts balanced strategic fit with near-term complexity and leverage. Meanwhile, Bernstein in July flagged incremental debt and integration risk versus strategic upside, highlighting $4 billion cash to BD and about $4 billion new debt at Waters.

Danaher, in its July 22, 2025 results, kept full-year 2025 core revenue growth at ~3% and raised adjusted EPS guidance to $7.70–$7.80; on the call the CFO said the company was “still at, you know, kind of a couple hundred million dollars of exposure right now today,” down from a prior about $350 million sizing. Agilent, on May 28, said “we estimate that the gross incremental tariff exposure in the second half of our fiscal year is $50,000,000,” and, if a 50% U.S. tariff on EU-sourced goods had begun July 9, that would add another roughly $40 million, but “we anticipate the net impact would be minimal,” and the firm expects to fully mitigate in FY26 via pricing and supply-chain moves.