In May 2015, the MIT Energy Initiative released a study on “The Future of Solar Energy” to assess how solar energy could grow efficiently and robustly in the U.S., as a key enabling technology for addressing climate change. Only two and half years have passed, but in the fast-moving world of renewable energy, that’s enough time for major changes.

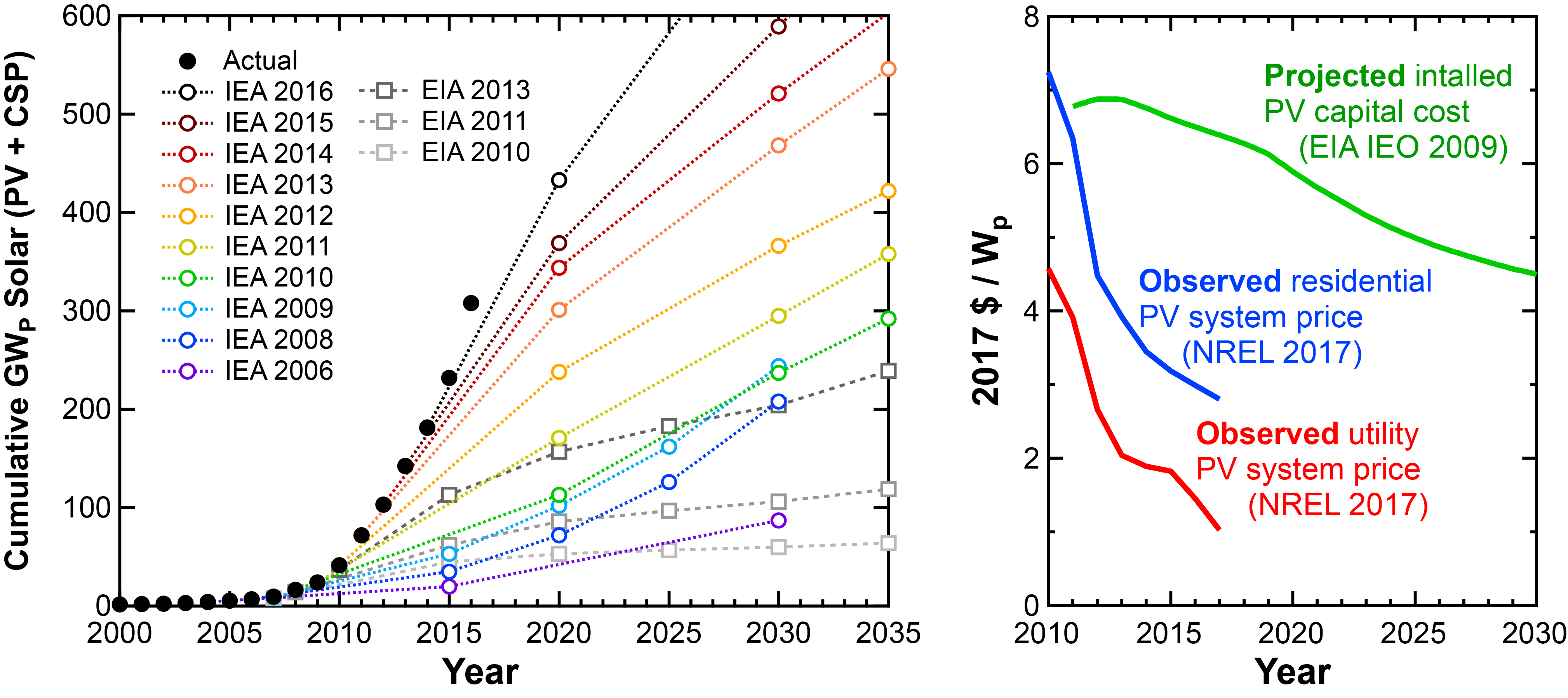

While the Future of Solar study did not try to predict the cost or deployment levels of solar power, we did observe a general trend: the cost of solar power tends to be lower than expected, and the deployment of solar power tends to be higher than expected (Figure 1, with data from IEA, EIA, and REN21 reports)—thanks to the low costs and the continued or strengthened contribution of deployment support policies. For example, the U.S. Department of Energy’s seemingly ambitious 2020 SunShot target of $1/WDC for utility-scale solar was met this year, three years ahead of schedule. Even the Future of Solar study did not anticipate the continued cost reductions for utility-scale solar plants: The DOE’s estimate of the unsubsidized levelized cost of electricity (LCOE) for new utility-scale solar plants today—5.0¢/kWh in the Southwest and 6.6¢/kWh in the Northeast—is less than half our estimate from 2.5 years ago (10.5¢/kWh in the Southwest and 15.8¢/kWh in the Northeast). Solar electricity is now slightly cheaper than natural gas and far cheaper than coal.

(left) Worldwide solar deployment (black circles, REN21) has consistently beaten projections (empty symbols with dotted lines), requiring these projections to be revised upward each year. “IEA” refers to “reference scenario” projections from International Energy Agency World Energy Outlook reports published from 2006-2016; “EIA” refers to the Energy Information Administration International Energy Outlook reports published from 2010-2013. (right) The cost of PV installations has similarly dropped much faster than projected. The projection denoted by the green curve is from EIA’s International Energy Outlook 2009 report; observed prices for residential- and utility-scale systems are from NREL 2017.

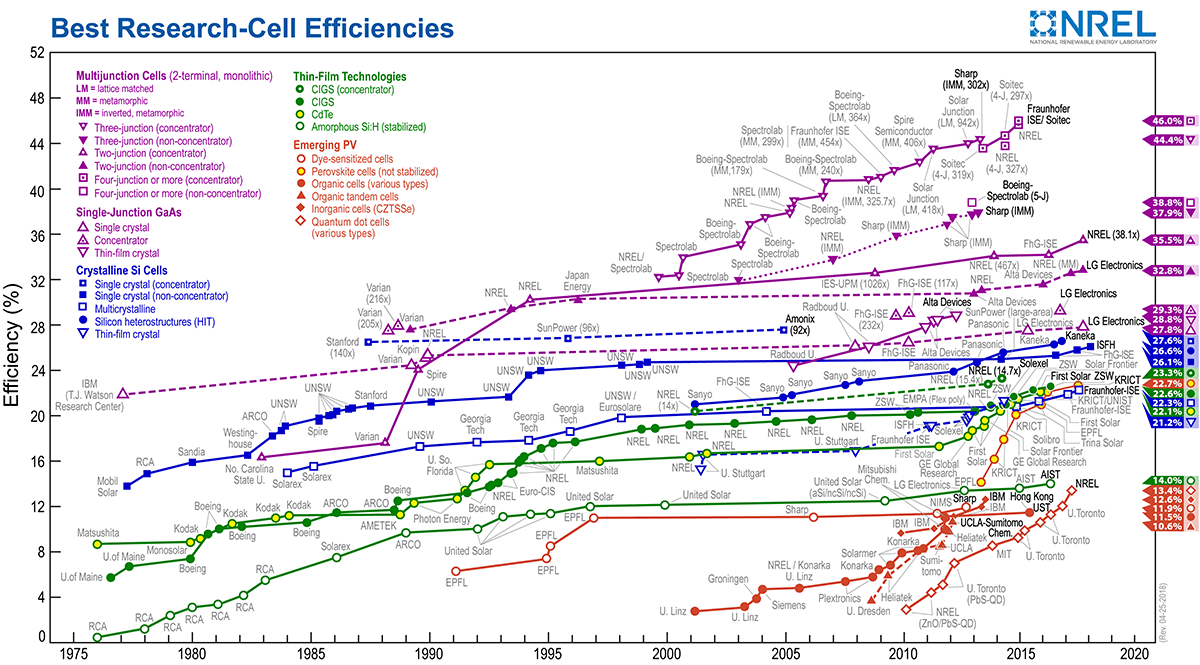

These cost reductions have resulted from improvements throughout the solar cost stack. While photovoltaic (PV) module cost reductions have dominated total cost reductions over the past 40 years—modules now cost about 200 times less in real terms than in 1978—further reductions since 2010 have been evenly split between the panel and balance-of-system components (everything else in the system, from racking, wiring, and inverters to installation labor, permitting, and overhead).

With module costs accounting for a shrinking fraction of system costs, future savings for silicon PV will continue to depend on both module performance improvement and balance-of-system innovation. In the DOE’s post-2020 roadmap for reaching an even more ambitious LCOE target of 3¢/kWh across the U.S., reductions in labor costs, financing rates, and operations & maintenance requirements are just as important as improvements in module efficiency and lifetime. In the face of threatened module tariffs, politically motivated electricity market distortions, and an ever-shifting regulatory landscape for distributed solar, long-term policy certainty could substantially improve the bankability of solar projects.

While crystalline silicon PV is likely to remain dominant for the next decade or more, rapid progress has been made in another solar cell technology: metal halide perovskites. Perovskite thin-film solar cells have improved faster than any other PV technology in history, rising from a record cell efficiency of 3.8% in 2009 to 22.7% today – higher than cadmium telluride (CdTe), today’s leading thin-film PV technology. And while the long-term stability of perovskites under operational and environmental stresses is still in question, recent progress in improving cell stability is promising. Many research labs around the world are now working toward uniform, high-throughput, large-area cell and module fabrication, a key step toward commercialization. Perovskites have the potential to reach a lower ultimate cost floor than silicon and to enable new deployment modes and applications with lightweight and flexible modules.

But perovskites don’t have to compete with silicon directly – the first application of perovskites may be to literally piggyback on top of silicon cells. Research groups at MIT, Stanford, and elsewhere have demonstrated perovskite-silicon tandems, layering a perovskite cell absorbing visible light on top of an infrared-optimized silicon cell. This approach could boost the efficiency of silicon cells by a few percentage points, potentially allowing the use of cheaper but lower-quality silicon feedstock that would otherwise be discarded. Several startup companies are already working to commercialize perovskite-silicon tandem solar cells.

With a clear roadmap for future advances, the cost of solar will likely continue to decline. But with solar PV at grid parity in many locations worldwide, the future of solar is likely to depend just as much, if not more, on the behavior of the rest of the energy system as on improvements to solar technology itself.

The Future of Solar study and other analyses from Lawrence Berkeley National Lab, the Potsdam Institute for Climate Impact Research, and others have identified one key defining challenge for future solar deployment, resulting from solar’s intermittent nature: as the penetration of solar power increases, the market value of solar electricity continuously declines. (Power prices are determined by the cost of supplying an additional unit of electricity from the cheapest remaining idle generator. Since solar always generates at zero marginal cost, the price of electricity at times when solar is generating – and thus the revenue that a solar generator receives – drops as more solar is deployed and more expensive generators are displaced.) The rate of value decline depends closely on the characteristics of the power system. Systems with lots of flexibility – characterized by a diverse mix of resources, a small fraction of must-run baseload power, robust transmission networks between neighboring regions, and energy storage resources – are best able to squeeze value out of each megawatt of solar capacity. Policies that encourage price-responsive electricity demand by passing the time-varying cost of electricity through to consumers (particularly if the social costs of carbon and air pollution are included) ensure that everyone can benefit from cheap solar electricity.

Similarly, one way to support solar growth is to support the growing electric vehicle market. If vehicle charging at mid-day (when solar is generating) is encouraged — supported by expanded workplace charging infrastructure and appropriate time-varying incentives — solar providers and electric vehicle users both win. Even without changes to charging infrastructure, deploying more electric vehicles would drive down the cost of battery systems through economies of scale and learning-by-doing, assisting the eventual grid-scale deployment of energy storage that would be needed to support high levels of solar generation.

Some regions of the U.S. are already getting appreciable amounts of electricity from solar – California generated almost 13% of its electricity from solar in 2016, and up to 23% in some 24-hour periods. The DOE’s recent report on grid reliability found variable renewables not to be a threat to grid stability and reliability, and earlier DOE reports found that at least 30% wind and solar can be integrated onto today’s grid without substantial changes to grid structure or operation. The U.S. as a whole only gets around 1% of its electricity from solar, so there’s plenty of room for expansion. And while debate continues over the merits and challenges of a 100% renewable energy system, many studies have shown that we can decarbonize the U.S. power system by at least 80% using today’s technologies.

While significant, long-term funding for basic research and development will always be important, the urgency of mitigating climate change means that we don’t have time to wait for the next generation of technology before rapidly scaling up solar generation. And with solar rapidly becoming the cheapest source of electricity in more and more parts of the world, we should deploy current solar technologies far and wide today, even as we continue to develop the technologies of tomorrow.

The MIT Center for Solar Energy Research, one of eight Low-Carbon Energy Centers developed by the MIT Energy Initiative (MITEI), focuses on technologies across a broad range of time horizons, from today’s commercial technologies to long-term, high-risk, transformational approaches, in all cases investigating ways to make solar energy technologies that are cheaper to manufacture, easier to deploy, and more power-efficient than those currently on the market.

The center works to overcome the barriers to worldwide deployment of solar power generation—from the nanoscale construction of better photovoltaic materials to addressing policy, regulatory and economic considerations to enable broad integration of solar power systems into the electric grid. The center brings together experts across 14 MIT departments. Working in close collaboration with MITEI’s members from industry, government, and the philanthropic and NGO communities enables the center to address these challenges on multiple technology and policy fronts simultaneously—ensuring progress is made toward deployable solutions that can meet global energy needs within the context of a carbon-constrained world.

About the Authors

Patrick Brown – Postdoctoral Fellow, MIT Energy Initiative

Joel Jean – Executive Director, Tata-MIT GridEdge Solar research program, MIT

Francis O’Sullivan – Director of Research, MIT Energy Initiative

Raanan Miller – MIT Energy Initiative; Executive Director Solar Energy Study

{kind=link}