2025 has not exactly been a good year for life science labs. While the pandemic gave rise to something of a lab sugar rush, lab funding was already down at the start of 2025 and the downward trend has mostly accelerated since then. A wave of speculative deliveries met softer demand, pushing national vacancy higher even as pricing and pipelines adjust. Things are looking up after the nadir. As the CBRE Q3 U.S. Life Sciences Figures Report, summarizes: “The overall lab/R&D vacancy rate for the top 13 life sciences markets rose slightly to 23.4% in Q3, largely due to the delivery of speculative space in three markets.” Average triple-net asking rent “fell to $70.42 per sq. ft. from $71.77 in Q2,” while “absorption turned positive for the first time in 2025 at 938,000 sq. ft. due to a slight increase in new leases and expansions.”

2025 has not exactly been a good year for life science labs. While the pandemic gave rise to something of a lab sugar rush, lab funding was already down at the start of 2025 and the downward trend has mostly accelerated since then. A wave of speculative deliveries met softer demand, pushing national vacancy higher even as pricing and pipelines adjust. Things are looking up after the nadir. As the CBRE Q3 U.S. Life Sciences Figures Report, summarizes: “The overall lab/R&D vacancy rate for the top 13 life sciences markets rose slightly to 23.4% in Q3, largely due to the delivery of speculative space in three markets.” Average triple-net asking rent “fell to $70.42 per sq. ft. from $71.77 in Q2,” while “absorption turned positive for the first time in 2025 at 938,000 sq. ft. due to a slight increase in new leases and expansions.”

A tenant’s market, but not an easy one

In top hubs, availability is high yet uneven by quality and readiness. The Bay Area sits near 30% vacant, according to Cushman & Wakefield’s Q3 read. Boston–Cambridge vacancy has hovered in the mid- to high-20s depending on the slice and source, with Savills noting 26.6% in Q3 and CBRE flagging a 27.7% high tied to speculative deliveries, San Diego has climbed as well, with Savills placing Q3 vacancy at 29.2%. New York remains elevated around 30.8%, per Savills’ Q3 update.

Landlords are leaning on concessions and tenant improvement packages to close deals, yet effective rent math still matters for budget-stretched teams. Multiple brokerage summaries and trade coverage note free rent and TI enticements rising even as asking rents drift lower, as Facilities Dive noted. In parallel, demand has shifted toward fitted, plug-and-play labs that shorten the time from lease to first experiment.

By the numbers (Q3 2025)

- Top 13 markets: Vacancy 23.4%; average asking rent $70.42 NNN; net absorption +938,000 sq. ft.

- Pipeline: 5.9 million sq. ft. under construction, ~57% preleased; under-construction volume down ~30% quarter over quarter.

- VC and employment: Life sciences VC $5.9 billion in Q3; YTD below 2024 but above 2019; biotech R&D and total life sciences employment stable through July.

- Market highlight: “Greater Los Angeles’s vacancy rate fell to 3.5%, including owner-occupied property, underscoring the market’s supply imbalance.”

Capital flows and demand are out of sync

Venture capital is recovering unevenly, with a structural shift toward AI, automation and robotics that is crowding out traditional lab-based discovery. Crunchbase reports that AI captured 33% of all global venture funding in 2024, totaling over $100 billion, up 80% from 2023. Meanwhile biotech’s share of U.S. startup funding fell to roughly 8%.

AI funding was already strong before ChatGPT hit the scene in 2022. But since then, AI along with automation and robotics, have grown so dominant that capital available for early-stage discovery companies with traditional wet-lab footprints has been squeezed. JLL data reveals a parallel trend: even within biotech, funding increasingly favors AI-native companies that require less physical lab space per employee. First-round financings for traditional biotech startups plummeted from $2.6 billion in Q1 2025 to $900 million in Q2, the lowest quarterly total in five years, according to HSBC. Meanwhile, Fierce Biotech reports that life sciences layoffs continue at last year’s pace.

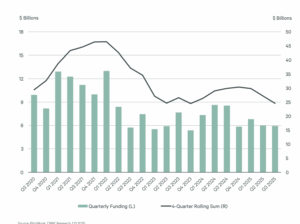

U.S. life sciences venture funding fell to $5.9 billion in Q3 2025, down $2.6 billion year-over-year and $43 million from the prior quarter, according to PitchBook and CBRE Research. While year-to-date totals remain above 2019 levels, the sector has declined steadily from its Q1 2021 peak of approximately $17 billion per quarter.