Intel’s potential split into design and fab fiefdoms under Broadcom and TSMC echoes a notable trend shaking conglomerates—think Honeywell’s fresh February 2025 plan to fracture into three, General Electric’s 2021 trilogy of aerospace, healthcare, and energy, or even semiconductor stalwarts like NXP shedding its Standard Products unit in 2016 to sharpen its chipmaking edge. For R&D pros, these breakups signal a growing trend, shrinking to greatness.

Intel’s potential split into design and fab fiefdoms under Broadcom and TSMC echoes a notable trend shaking conglomerates—think Honeywell’s fresh February 2025 plan to fracture into three, General Electric’s 2021 trilogy of aerospace, healthcare, and energy, or even semiconductor stalwarts like NXP shedding its Standard Products unit in 2016 to sharpen its chipmaking edge. For R&D pros, these breakups signal a growing trend, shrinking to greatness.

But there’s more to the story than carving up bulging businesses that had sprawled over the decades. President Donald Trump’s proposed tariffs on Taiwanese semiconductors—ranging from 25% to up to 100%—aim to force chip production back to U.S. soil. Taiwan’s TSMC, which produces the majority of the world’s latest chips (including NVIDIA’s GPUs), is squarely in the crosshairs. These tariffs, if enacted, would hike costs for a swath of U.S. importers ranging from NVIDIA to Apple and AMD. Such moves could also disrupt supply chains and inflate prices for GPUs, smartphones and beyond.

The potential of splitting Intel’s design and fab

Enter Intel, whose potential split into design (under Broadcom) and fabrication (under TSMC) mirrors Honeywell and GE’s strategic fractures outside of the semiconductor space. Intel’s breakup would end Intel’s long-held integrated device model (IDM), creating separate design and fabrication entities.

Broadcom’s interest would lie in acquiring Intel’s CPU and GPU design teams—responsible for Xeon server chips and emerging AI accelerators like Gaudi—to directly challenge NVIDIA’s AI dominance. Analysts like Bernstein’s Stacy Rasgon suggest this would instantly transform Broadcom into a full-stack data center contender, pairing its networking application-specific integrated circuit (ASICs) with Intel’s x86 expertise. While Broadcom’s CEO, Hock Tan, in December dismissed the possibility of a hostile takeover of Intel, the company has apparently warmed up to the idea since, according to WSJ.

This potential Intel breakup also lands amidst a growing push for U.S. semiconductor independence. With geopolitical tensions rising and supply chain vulnerabilities exposed in recent years, Washington is actively incentivizing domestic chip manufacturing. Were TSMC to acquire Intel’s fabs, even partially, it could be a strategic win for U.S. onshoring efforts, ironically with foreign entity orchestrated it. There is precedent here too. Last year, TSMC began producing chips for Apple at one of its Phoenix semiconductor chip factories, according to media reports. TMSC’s counts the facility as among the world’s most advanced for semiconductor technology.

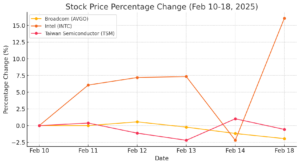

Investors apparently like the idea of splitting up Intel, judging by the stock market’s reaction to the news. Its shares jumped 16% on Tuesday. Broadcom and TSMC shares are mostly holding steady.

Aiming to break NVIDIA’s hardware hold

Intel’s aim to be both a leading chip designer and a top-tier manufacturer has increasingly run aground—especially as pure design rivals like NVIDIA and pure fabrication giants like TSMC advance unabated. According to CRN, Intel acknowledges that specializing—whether in design or fabrication—could be the only way to recapture its edge. By offloading its fabs to TSMC and funneling its CPU and GPU design teams into Broadcom’s ecosystem, Intel would effectively emulate the “split-to-thrive” approach reshaping that has become more common over the years with conglomerates.

![Intel Core Ultra 200S series processor family [Intel]](https://www.rdworldonline.com/wp-content/uploads/2024/11/newsroom-intel-arl-chip-4_1920-1080-300x169.avif)

Intel Core Ultra 200S series processor family [Intel]

With Intel’s design teams potentially under Broadcom’s disciplined, profitability-driven culture, the company might shift Intel’s design unit to market-driven R&D, narrowing around datacenter and AI accelerators that directly challenge NVIDIA. Broadcom, historically focused on networking chips, with little presence in CPUs/GPUs, might see in Intel’s x86 capabilities a chance to fuse CPU and GPU synergy with its ASIC experience. On the fabrication side, TSMC’s proven process technology could also breathe new life into Intel’s fabs.

Broadcom would see benefits, too

Despite major AI investments, Intel hasn’t managed to challenge NVIDIA’s dominance. But as Ctech notes, Broadcom’s potential acquisition of Intel’s design teams could change that. By combining Broadcom’s custom silicon expertise for hyperscalers with Intel’s CPU/GPU IP, a formidable full-stack AI competitor could emerge—even as customers like Google (with its TPUs) and Meta (with its MTIA) develop their own AI chips.

Meanwhile, TSMC acquiring Intel’s fabs would leave Samsung as the last major integrated chip designer-manufacturer. For Intel, whose stock dropped 40-60% last year before recently rebounding 30% on split rumors (see graph above), this isn’t just another conglomerate carve-up—it’s a bid to regain relevance in a fast-growing semiconductor market. While AMD and NVIDIA might gain short-term advantage during the transition, they could soon face a reinvigorated Broadcom-Intel competing for AI and data center dominance.

Success, however, is not guaranteed

While a Broadcom-Intel partnership underpinned by TSMC’s US fabs could, in theory, mount a serious challenge to NVIDIA’s dominance, success is far from assured. NVIDIA’s ecosystem lock-in—driven by CUDA’s deep developer adoption and a robust AI software stack—remains a formidable barrier to entry. Broadcom’s acquisition track record shows it can integrate and streamline operations, but transforming Intel’s design heritage into a true AI powerhouse will require more than just cost advantages or a broader product portfolio.

| Metric | NVIDIA | Potential Broadcom-Intel factors |

|---|---|---|

| Market Focus | GPUs, AI accelerators, CUDA ecosystem | CPUs, GPUs, AI accelerators, networking |

| Software Ecosystem | CUDA, strong developer adoption | OpenVINO, oneAPI, less adoption |

| Manufacturing | TSMC (Taiwan) | TSMC (US fabs, potential tariff avoidance) |

| Recent Performance | $30B Q2 revenue, 122% growth | Gaudi missed $500M target in 2024 |

| Strategic Advantage | First-mover in AI, ecosystem lock-in | Cost advantage from US manufacturing |

At the same time, looming tariffs could reshape the economics of chipmaking in favor of local production. If Broadcom and TSMC successfully navigate these policy shifts, their newly specialized approach for AI-hungry hyperscalers. But a shifting tariff landscape could also lead NVIDIA to potentially avoid US tariffs on Taiwanese semiconductors by shifting production to TSMC’s facilities in the U.S., such as the Arizona fab, which supports the 5 nm and 4 nm processes needed for NVIDIA’s GPUs like the H100. Yet capacity constraints at TSMC’s US fab could limit NVIDIA’s ability to fully relocate production (TSMC’s Arizona fab has an estimated capacity of 20,000+ wafers per month), meaning they would likely still face tariffs on chips imported from Taiwan given the overwhelming demand for their latest-gen GPUs. Whether Intel’s transformation is enough to unseat market incumbents like NVIDIA depends on execution and the ever-evolving demands of next-generation AI workloads.